PKU's Huang Yiping: China's Demand Problem Can No Longer Wait

Dean of the National School of Development argues China's "strong supply, weak demand" imbalance now demands a coordinated five-part fix, not a single stimulus lever

For today’s episode, I bring the latest analysis from Professor Huang Yiping. He is the Dean of the National School of Development at Peking University and also a member of the People’s Bank of China’s Monetary Policy Committee.

Professor Huang has long been one of the most influential voices in China’s economic policy debates; he briefed Premier Li Qiang in 2023 during the economic situation symposium.

Huang argues that the very nature of China’s economic imbalance has changed. China has shifted from a small-country to a large-country economy; combined with rising trade barriers abroad, this means the old escape valve—exporting excess capacity—is closing fast. He suggests that expanding domestic demand has switched from a long-term goal to a short-term urgency. Signs of that are also shown in the difference between the 15th Five-Year Plan and the Central Economic Work Conference; the 15th Five-Year Plan puts forward two important tasks—developing new quality productive forces and expanding domestic demand—and the Central Economic Work Conference reversed their order, which suggested expanding domestic demand is now the priority.

He also calls for a fundamental rethink of how policy is designed: not a single stimulus lever, but a coordinated combination that simultaneously lifts demand in the short run and removes the structural roots of weak consumption over the long run.

Some other highlights:

China is already rebalancing—just not enough. Huang pushes back against the common perception that no progress has been made. He points to consumption rising from 49.6% of GDP in 2010 to 57.1% in 2024, investment falling, and the current-account surplus dropping from its 2007 peak. Yet, with consumption still below 60% compared with a global average of around 75%, the work is far from done.

The roots run deep. He traces “strong supply, weak demand” to a high savings rate, “asymmetric marketization” that suppressed factor prices for decades, local governments’ GDP-driven preference for investment over consumption, and a labor market that failed to translate growth into proportional gains in household income.

A five-part policy combination. Huang argues that, unlike the Asian financial crisis era, strong macro stimulus alone won’t work, and lays out a coordinated package:

Macro policy should turn genuinely expansionary, but with the firepower aimed at households rather than at new investment projects—channeled through social security, welfare benefits, and direct transfers so that stimulus actually reaches consumers.

Market-oriented reform should finish the unfinished business of factor-price liberalization, correcting the “asymmetric marketization” that long held down the cost of capital, land, and labor at households’ expense, while restoring private-sector confidence.

Balance-sheet restructuring should address the strained balance sheets of local governments, property developers, and households, since over-indebted actors cut spending no matter how loose policy becomes.

“Investing in people” should expand public services and the social safety net—covering migrant workers through hukou and social-security reform in education, healthcare, and pensions—to lower precautionary saving and free up income for consumption.

A more responsible international role matters because structural contradictions should be resolved through domestic public policy rather than trade restrictions—yet other countries’ choices are beyond China’s control. With China’s export increase now drawing pushback, it must manage trade frictions rather than rely on overseas markets to absorb excess capacity.

Income and confidence are the bottom line. Drawing on his own online consumer-brand research, Huang concludes that reviving consumption ultimately comes down to two things: people having money to spend, and daring to spend it.

Thanks Dr.Huang for authorizing me to translate his latest analysis into English. Below is the translation I made:

Policy Approaches Under the Macro Pattern of “Strong Supply, Weak Demand”

The Economic Growth Model

In his opening address at the Summer Davos Annual Meeting in 2007, Premier Wen Jiabao noted: “The overall situation of China’s current economic development is good. At the same time, there are also some problems in economic development that are unstable, uncoordinated, unbalanced, and unsustainable—mainly an excessively fast pace of economic growth, prominent structural contradictions, an extensive mode of development, excessive resource and environmental costs, mounting pressure of rising prices, and institutional and mechanism-related obstacles that have not yet been fundamentally eliminated.”

Twenty years have passed, and many of the issues now under heated discussion seem to bear similarities to those raised back then.

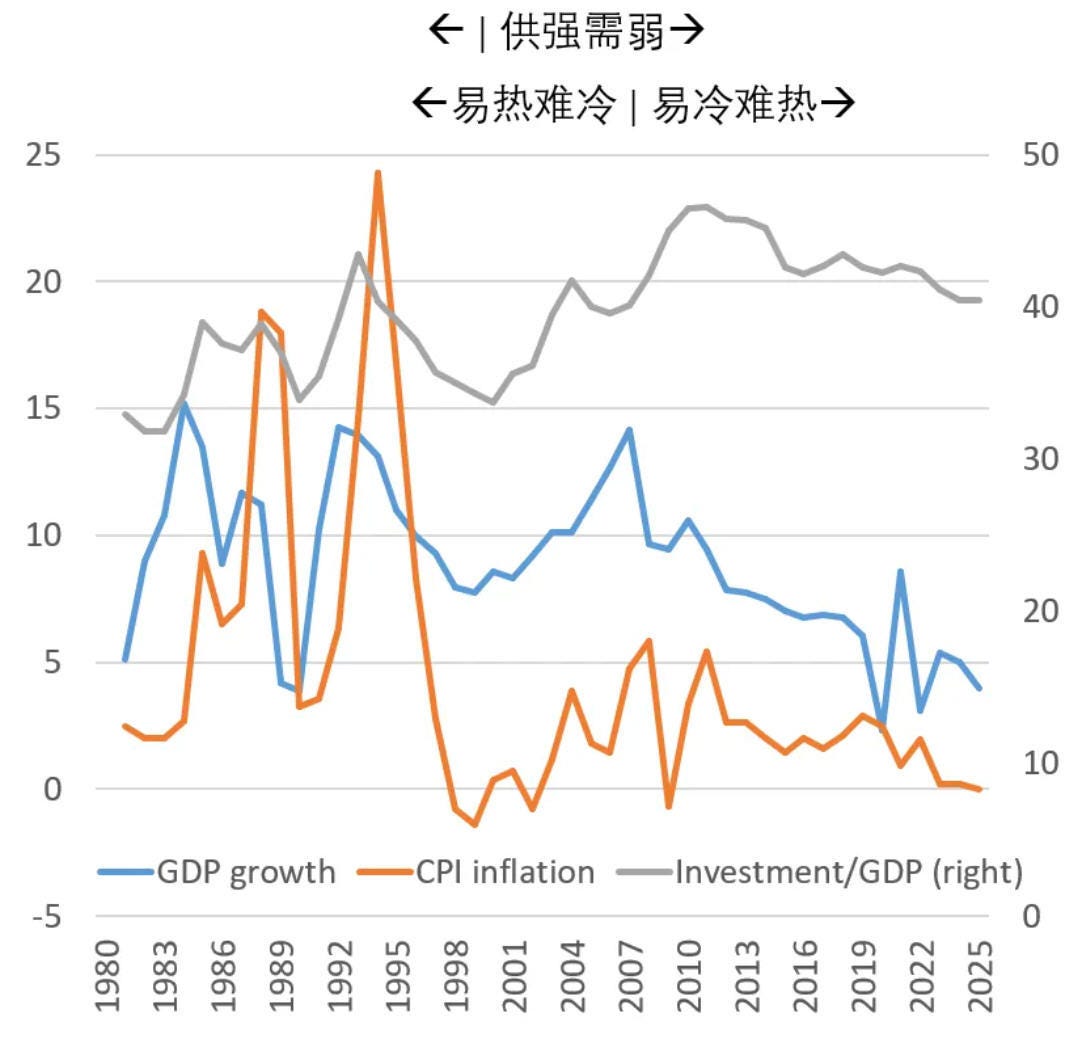

From the trends of the GDP growth rate and CPI in Figure 1, one can clearly observe phased changes. Roughly divided by time period: after the Asian financial crisis, the relationship between supply and demand began to exhibit the characteristics of “strong supply, weak demand.” Before that, China’s economy frequently faced high inflationary pressure; afterward, inflationary pressure weakened significantly, which to some extent reflects a shift in the supply-demand pattern.

Another key turning point appeared after the global financial crisis. Before it, China’s economy as a whole displayed the characteristic of being easy to overheat and hard to cool down; after the crisis, it shifted to being easy to cool down and hard to heat up, with the economy continuously facing downward pressure. At the policy level, growth-stabilization measures were introduced on multiple occasions, but after growth briefly stabilized for a period, new downward pressures would emerge again.

The core feature of the current macroeconomy is precisely this tendency to cool easily and heat with difficulty; viewed from the perspective of supply and demand, it is concentrated in the form of strong supply and weak demand.

Data on manufacturing capacity also corroborate the feature of strong supply and weak demand: China accounts for more than 30% of global manufacturing, ranking first in the world for 15 consecutive years. Of the world’s 500 categories of manufactured goods, China ranks first globally in production capacity for 220 of them. Looking at the manufacturing capacity utilization rate for 2025: China stands at 74.8%, the United States at 76.8%, Germany at 77.7%, Japan at 76.3%, and the global average at 78.2%. The gap between China and the major economies, as well as the global average, is not large, but overall it remains slightly on the low side.

The Causes of “Strong Supply, Weak Demand”

There are many reasons for the formation of the “strong supply, weak demand” pattern, and these reasons are not mutually exclusive or independent of one another—many are in fact interconnected and mutually influential.

1. High Savings Rate

First, the high savings rate is both an important cause of the current “strong supply, weak demand” pattern and, one could say, an intuitive result of this pattern. As Figure 2 shows, China’s gross national savings rate is at a very high level among the major economies. There is also one country with an even higher savings rate that is not listed—Singapore, at roughly around 50%.

If gross national savings is divided into the household sector and the public sector, one finds that China’s household-sector savings rate is indeed on the high side, at roughly 35% in the 2024–2025 data. However, compared with other East Asian economies, the gap is not particularly significant—for example, Indonesia’s household savings rate also reaches 35%, and many other economies are likewise at relatively high levels.

Some attribute this to Eastern culture’s reverence for saving and emphasis on long-term planning. I do not deny the influence of such cultural factors. But the high household savings rate clearly has other causes as well—for instance, the social security system is not yet well developed, so households need to rely more on their own savings to guard against future risks.

Although the household savings rate is high, the difference from other countries is not particularly pronounced. Another very important reason why China’s overall gross national savings rate is high is that the public sector accounts for a relatively large share of national income. For example, after a local government obtains a sum of land-transfer revenue, the proportion used for direct consumption is usually very low. Therefore, the public sector’s extremely high savings is an important factor pushing up China’s gross national savings rate.

2. Distortions in Factor Markets

More than a decade ago, we conducted related research and discovered a very distinctive phenomenon in China’s reform process, which we called “asymmetric marketization.” Since economic reform was launched in 1978, China’s overall direction has always been toward marketization, but the pace of marketization has been uneven across different domains. The core manifestation of so-called asymmetric marketization is this: the product market was largely and comprehensively liberalized fairly quickly, while distortions in factor markets remained relatively prominent. In the financial field that I follow, this feature is especially evident. The “financial repression index” shows that China’s index is significantly higher than that of most countries in the world, which to some extent reflects the considerable degree of government intervention that still exists in the financial system.

The fact that factor markets were not liberalized in step has multiple underlying causes, closely related to the gradualist, dual-track approach to reform that China adopted in the early period of reform. One important reason for adopting dual-track reform was to avoid the shock-therapy approach of liberalizing everything at once; the cultivation and refinement of market mechanisms is a gradual process, and abrupt, comprehensive liberalization tends to deviate from the intended objectives. The logic of the dual-track system is to retain the operation of the old system while liberalizing a new market track, gradually pushing the old track to converge with the new track and eventually merging the two. This model was once widely applied across many domains.

The advantages of this model are obvious: maintaining overall stability during economic transition, avoiding economic chaos caused by the sudden exit of the old system before the new mechanism has fully taken shape—this is crucial for a smooth transition. But it also has clear shortcomings: it brings about a certain loss of efficiency, and the coexistence of dual tracks easily breeds arbitrage behavior. How to continue deepening reform is a challenge we face over the long term.

Gradualist dual-track reform means that the old track needs to keep operating for a considerable period of time, and since the old track is inherently less efficient than the new track, ensuring its smooth operation objectively requires corresponding subsidies. And given limited fiscal resources, the most direct way is to suppress factor prices through distortions in factor markets, providing support in a disguised form. For example, in the early stage of reform, banks channeled low-cost credit on a large scale to state-owned enterprises—essentially a form of non-fiscal, implicit support.

In 2010, Tao Kunyu and I found in our research that factor-market distortions in 2009 were equivalent to 5.1% of GDP. According to a 2022 report by the team led by Gerard DiPippo at the U.S. think tank CSIS, which estimated the broad-caliber ratio of industrial subsidies to GDP (2019 data), China’s figure was 4.9% and the United States’ was 0.39%. Their estimates do not differ much from our calculations, but I do not agree with their simplistic characterization of attributing the entire amount to industrial subsidies. There is indeed a certain degree of industrial-subsidy behavior in localities’ investment-attraction efforts, but the underpricing of factors is, to a much greater extent, the cost paid for economic transition—an implicit burden-sharing during the transition process, rather than simply industrial support.

If one accepts this judgment of asymmetric marketization—that product prices were comprehensively liberalized while factor-market distortions have long existed and have not yet been fully eliminated to this day—then it means factor prices have generally been suppressed, which amounts to implicit support for producers, investors, and exporters over a very long period. And those who bear this portion of the cost are precisely the owners of the factors, primarily the household sector. This distinctive reform strategy has objectively formed a redistribution of income between producers and consumers. From this perspective, the “strong supply, weak demand” pattern has an intrinsic connection with the particularity of China’s reform strategy or path.

3. Local Governments’ Pursuit of Growth

As is well known, in the early period of reform China implemented decentralization reforms, devolving a great deal of resource-allocation authority from the central level to localities. This greatly mobilized localities’ enthusiasm for developing the economy and also allowed localities to formulate economic policies according to local realities. At the same time, competition among regions centered on GDP growth significantly boosted overall economic vitality, with local governments playing a key role.

For a very long time, local officials in charge were like CEOs of their regional economies, with their core work being to attract investment and advance construction. On the positive side, this did indeed powerfully drive economic growth—that is an objective fact; but at the same time, the tendency in the development process to emphasize investment and neglect consumption was also very prominent.

Consider this: after a local government obtains a sum of land-transfer revenue, is it more inclined to use it to drive consumption or to invest it in construction? Objectively speaking, in choosing the path of economic growth, stimulating consumption is slow to take effect and difficult, whereas investing in building infrastructure, creating industrial parks, and advancing industrialization yields quick results and provides tangible levers. This behavioral pattern was continuously reinforced, ultimately further intensifying the overall “strong supply, weak demand” pattern in the economy.

4. Wages Under a Labor Surplus

For a very long period in the past, China’s labor force was persistently in a state of surplus. In economies with abundant labor, the generally successful path to achieving economic takeoff is to start by exporting labor-intensive manufactured goods. In the first few decades of reform and opening up, we achieved tremendous success precisely by following this road. Not only mainland China, but also Japan, South Korea, and other Asian economies such as Taiwan, Hong Kong, and Singapore traveled similar development paths—that is, relying on abundant or even surplus low-cost labor to mass-produce labor-intensive products, forming significant competitiveness in international markets, and thereby driving export expansion and economic growth.

For a period of time, this model also brings about a typical consequence: because of the surplus supply of labor, wage levels are suppressed across the board. The economy was developing rapidly, yet wages failed to rise substantially in step, directly leading to the share of household income in national income falling rather than rising. This is also a phenomenon that many East Asian economies experienced in common during their high-growth stages—a declining share of household income and a correspondingly lower share of consumption in GDP. This pattern was also highly consistent with China’s economic structure at the time.

From the perspective of development economics, when the labor market shifts from surplus to shortage, the so-called “Lewis turning point” appears. Professor Cai Fang once judged that China roughly crossed this turning point around 2006. In other words, before 2006 the problem of labor surplus was very prominent, and after that this contradiction clearly eased. But now, when speaking of the job market, people’s intuitive feeling is that labor shortage is not prominent—indeed, quite a few people still face the pressure of unemployment.

5. Wage Income and Property Income

Over the past dozen or so years, innovations in digital technology—especially artificial intelligence technology—have to some extent had a substitution effect on labor. By the general rule, after the “Lewis turning point” labor wages should have risen substantially, thereby driving a significant increase in the share of household income in national income. But this phenomenon has not been evident over the past dozen years or so, and there are some special reasons behind it. Many trends that historically appeared in other countries have instead been less pronounced in China’s market—indeed, quite a few people still feel considerable employment pressure—which means that household consumption demand lacks strong income support.

There is also a view that, on the one hand, wage growth is weak, while on the other hand, against the backdrop of an aging population, society’s demand for property income is rising. In the future, as the labor force continues to shrink, wage levels will theoretically rise somewhat, but in addition to wage income, many people also need to rely on property income to support their livelihoods. If this portion of income cannot be effectively supplemented, it will likewise constrain the release of consumption demand.

6. Major Risk Factors

Major risk factors in economic operation have had a significant impact on the supply-demand relationship. Fluctuations in the real estate market affect the balance sheets of multiple economic sectors—including local governments, financial institutions, and the household sector—and their suppressive effect on aggregate demand, especially consumption demand, is very evident. The continued deepening of population aging puts long-term pressure on social security, the healthcare system, and government fiscal budgets. The strained finances of local governments have also, to a certain extent, affected infrastructure construction and the effective supply of public goods.

To summarize briefly: the current macroeconomy presents a “strong supply, weak demand” pattern, and the formation of this situation is the result of multiple factors working together. The several key causes just outlined can be summarized as follows:

First, the savings rate is high, with a correspondingly low share of consumption. Second, the past reform process had the characteristic of asymmetric marketization, with factor prices underpriced to a certain degree, further amplifying the “strong supply, weak demand” contradiction. Third, local governments have long been oriented toward GDP growth, and their tendency to emphasize investment and neglect consumption has aggravated this structural problem. Fourth, both before and after the “Lewis turning point” the labor market failed to drive significant and relatively rapid growth in household income, forming a clear constraint on consumption. Layered on top of these are multiple risk factors such as real estate, population aging, and local fiscal pressure. Overall, the feature of generally weak consumption demand in China over the past period has become very clear.

Already Rebalancing, but Not Enough

Many people have this question: Premier Wen pointed out problems with the economic growth model back in 2007, and in fact related discussions began even earlier—so why, even today, has the problem of structural imbalance still not been thoroughly resolved? In many people’s impression, the Chinese government has strong execution capacity and acts decisively, usually able to respond promptly when problems arise; yet on rebalancing and structural adjustment, no significant progress has been made for a long time. On this point, I do not fully agree.

Not long ago, the French presidency invited the Centre for Economic Policy Research (CEPR) to produce a study called the “Paris Report,” focused specifically on global economic rebalancing. France will host the G7 summit this year, and this report was prepared precisely for that purpose. In this report on global rebalancing, the organizers invited me to write the chapter on the rebalancing of the Chinese economy. The core argument I put forward first in the text is this: China’s economy has in fact already been rebalancing. Many foreign peers’ intuitive reaction to this judgment is one of disbelief.

But the economic data support my argument. The past economic structural imbalance, put simply, was that growth relied excessively on investment and exports while consumption was relatively insufficient. The indicator of this imbalance that draws the most external attention is the continued expansion of the current-account surplus and the trade surplus, with large amounts of domestic capacity being exported abroad.

Consider several sets of key data: First, the share of investment in GDP fell from 46.6% in 2011 to 40.6% in 2024. Second, the share of consumption in GDP rose from 49.6% in 2010 to 57.1% in 2024. Third, the share of the current-account surplus in GDP fell from 9.8% in 2007 to 2.3% in 2024. Although the share of the current-account surplus in GDP rebounded again after 2018, the ratio has remained at around 2% or below (3.7% in 2025).

At the time, the G20 Seoul Summit proposed a guiding range for external rebalancing—namely, that a surplus or deficit not exceeding 4% of GDP could be regarded as basically balanced. By this standard, China’s level in recent years has clearly been within the reasonable range. Since 2018, the share of China’s current-account surplus has rebounded somewhat, reaching 3.7% in 2025—a rebound from the previous few years, but still not touching the 4% warning line; this change, however, is worth watching.

Therefore, the rebalancing of China’s economy is in fact already happening, and great progress has been made compared with twenty years ago.

Of course, although rebalancing has made progress, it is still far from enough. At present, China’s share of consumption in GDP is about 57.1%, while the share of investment remains above 40%, and the contradiction of supply exceeding demand is still very prominent. From an international comparison, the global average consumption rate is about 75%, while China’s is less than 60%, indicating that consumption is still insufficient. Rebalancing still needs to be continuously advanced, and achieving a more balanced domestic supply-demand relationship in the future remains a major task.

Professor Helene Rey of London Business School once commented on my article, noting that China’s current-account surplus as a share of its own GDP is indeed declining—it has merely rebounded recently—but because the Chinese economy has grown so rapidly in scale, China’s surplus as a share of the GDP of the rest of the world or of its major trading partners may actually have risen. This means that, viewed from our own perspective, the relative proportion of external imbalance is declining; but from the trading partners’ perspective, the rise of China’s surplus relative to the size of other economies will increase the adjustment pressure on them. This is also a point we should take very seriously.

The Challenges of a Large-Country Economy

The outside world’s level of concern about our imbalance problem has not declined, and the core reason is that over the past twenty-odd years China has grown from a small-country economy into a large-country economy. No matter how a small-country economy’s imports and exports change, it can hardly affect the equilibrium of international markets; but having become a large-country economy, to put it colloquially, “whatever it sells becomes cheap; whatever it buys becomes expensive.” Even though China’s current-account surplus as a share of GDP has fallen and its own rebalancing has made progress, the rapid rise of its industries still brings tremendous adjustment pressure to other countries.

In early April 2024, then-U.S. Treasury Secretary Janet Yellen visited the National School of Development at Peking University, where she raised the question: with China’s new-energy vehicle scale so large, can the relevant U.S. industries still develop? She worried that large-scale capacity directed overseas would impact the U.S. auto industry, employment, and income distribution.

After World War II, when the United States led globalization, it advocated that countries divide labor based on comparative advantage, each doing what it does best for mutual benefit. But this set of ideas now faces challenges in reality, the key being that globalization is inevitably accompanied by structural adjustment. For example, China is good at manufacturing and Australia is good at growing grain, and trading with each other to exchange what one has for what one lacks is in itself win-win; but the problem that follows is: can Chinese farmers smoothly transition into manufacturing? Even if they can, the transition process is extremely difficult. The pain of such structural adjustment is a challenge that all countries face in common in globalization.

The U.S. problem is especially prominent. As an advocate of globalization and one of its biggest beneficiaries, the United States has a per-capita GDP that significantly leads other developed countries, yet it cannot escape structural difficulties either. Yellen specifically mentioned the employment plight of blue-collar youth in small American towns—something that has long gone beyond the economic sphere and evolved into a social and political problem. The emergence of anti-globalization policies in some countries is, to a large extent, precisely the externalization of domestic contradictions.

As an economist, my basic judgment is this: if a country concludes that globalization brings more benefits than harm overall, it should resolve structural contradictions through domestic public policy rather than simply resorting to trade restrictions. But the policy choices of various countries are not something we can control.

What needs to be made clear is that when an economy reaches a certain scale, changes in its supply and demand will significantly affect global markets and other countries’ decisions. Even if China’s current-account surplus share declines, it will still bring major adjustment challenges to many countries. In particular, China’s emerging industries are developing rapidly and its industrial chains are highly concentrated, so large-scale exports can very easily impact other countries’ industries. When countries generally worry about industrial security, employment stability, and income distribution, we, as a large-country economy, must consider how to develop in coordination with the world. A small country’s increased exports will be accepted, whereas a large country’s scale expansion will bring adjustment pressure—this is a new challenge we must face.

It is precisely for this reason that “strong supply, weak demand” has now become a prominent macroeconomic problem. But this is not a new problem. Since reform and opening up, overcapacity has appeared repeatedly. The former State Planning Commission (now the National Development and Reform Commission) issued warnings almost every year about overcapacity in certain fields and the need to avoid blind investment, and the governance of excess capacity also continued for many years—yet this did not prevent China from achieving high-speed growth averaging nearly 9% per year. The core reason is that in the past we were a small-country economy, and the domestic “strong supply, weak demand” gap was mainly absorbed through exports, forming an international grand cycle of “importing technology, capital, and raw materials from abroad, processing them, and exporting at low cost,” relying on external demand to absorb domestic excess capacity.

The situation now is this: on the one hand, the spillover effects of a large-country economy have triggered global vigilance, and other countries’ policy responses have clearly changed; on the other hand, countries are using trade measures such as tariffs to guard against market impacts. The room to balance domestic supply-demand contradictions by relying on exports has narrowed dramatically.

Although “strong supply, weak demand” is a long-term problem, its nature has fundamentally changed. In the past it was mainly a problem of structural rebalancing, a requirement for achieving long-term sustainable growth; now it directly bears on whether short-term growth can be stabilized. China’s capacity utilization rate is slightly below the global average, exports have remained strong in recent years, and the advantage of a complete manufacturing industrial chain is evident; but rapid export growth has simultaneously intensified external concerns—and not only in the United States and Europe.

The “15th Five-Year Plan” puts forward two important tasks—developing new quality productive forces and expanding domestic demand—and the Central Economic Work Conference reversed their order, with expanding domestic demand shifting from a long-term goal to a short-term and urgent task. If expanding domestic demand cannot take effect quickly and exports encounter obstacles again, large amounts of capacity may become substantively excess, in turn triggering risks to investment returns. General Secretary Xi Jinping published an important article, “Expanding Domestic Demand Is a Strategic Measure,” in the journal Qiushi, profoundly explaining the strategic significance of expanding domestic demand. How to effectively reverse the supply-demand imbalance is now the key to current economic work.

Shifting Toward the Domestic Grand Economic Cycle as the Mainstay—Developing New Quality Productive Forces and Expanding Domestic Demand

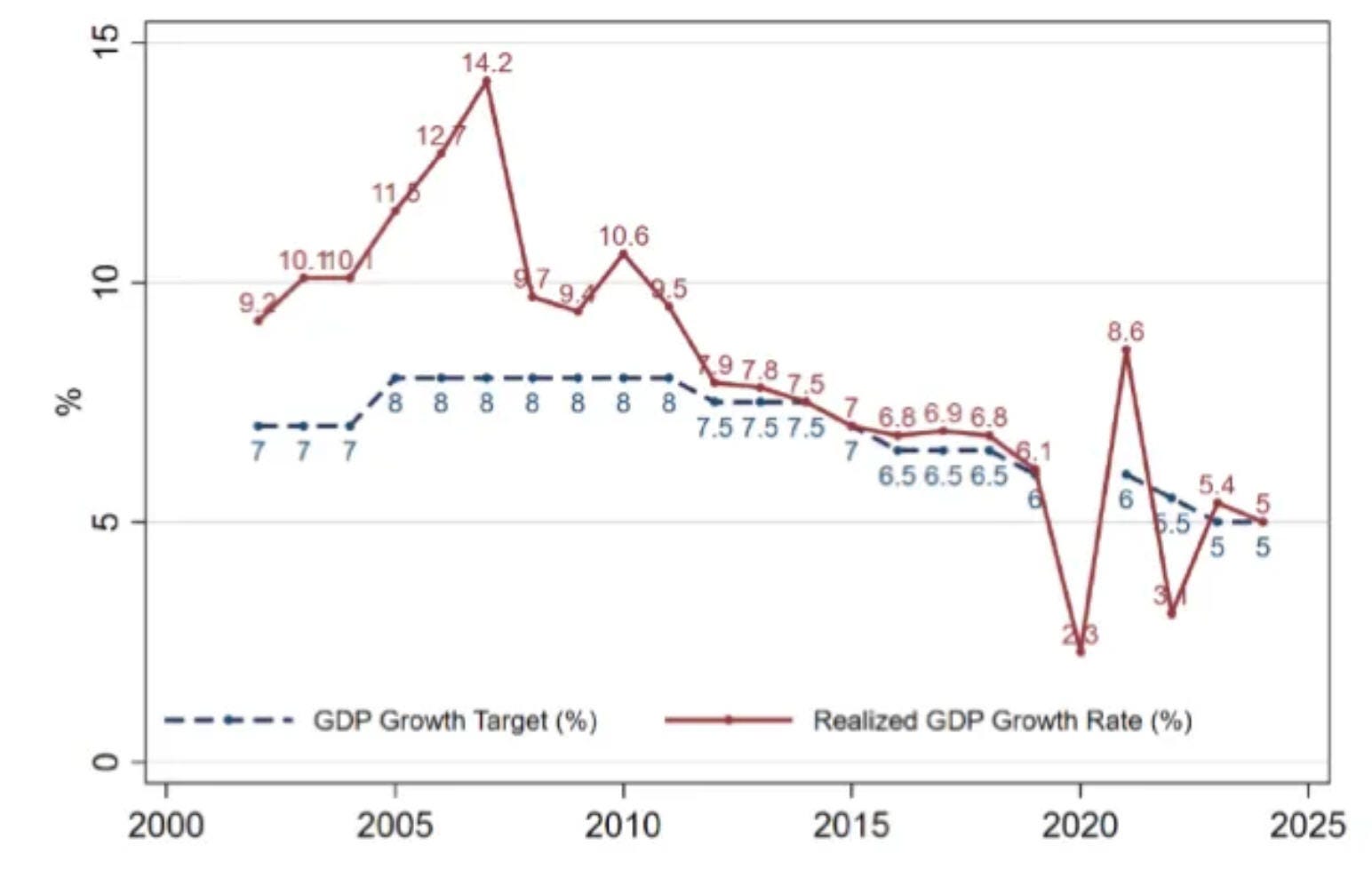

During this year’s Two Sessions, people noticed that the GDP growth target was adjusted from the previous “around 5%” to “4.5%–5%,” and I believe this adjustment is highly appropriate. Figure 3 is drawn from research by Professor Xiong Wei of Princeton University; the red line is the actual GDP growth rate each year, and the blue line is the annual growth target set at the Two Sessions.

In 2012 there was a clear inflection point: before that, the target was mostly set at around 8%, and the actual growth rate often substantially exceeded the target, making the task relatively easy to fulfill; after 2012, the growth target was continuously lowered, and the actual growth rate hugged the target tightly and closely.

In these years the growth target has had to be gradually lowered, and even so, ultimately achieving the target has often required going all out. And to ensure meeting the target for the current year, localities tend to adopt short-term measures that take effect quickly, and find it hard to lay out long-term reforms that are slow to take effect. This approach easily depletes future momentum and instead further intensifies downward economic pressure.

I strongly agree with moderately lowering the growth target, the essence of which is to leave room for transformation. I have recently been running with students and alumni, and I have a personal feel for this. Regular runners all know that starting too aggressively easily leads to running out of steam and crashing midway; only by slowing the pace at the beginning and laying a good foundation can you run longer and steadily pick up speed later. Economic development follows the same logic. From this perspective, this year’s target adjustment comes at exactly the right time. If we focus more energy on the two major strategic tasks—developing new quality productive forces and expanding domestic demand—and free ourselves from excessive pursuit of short-term speed, future economic growth will instead be more solid and more sustainable.

The new policy orientation is precisely to take the path of dual-circulation development, shifting from the past, where the international grand economic cycle was the mainstay, to the domestic grand economic cycle as the mainstay. Whether the domestic grand economic cycle can run smoothly hinges on getting two core links right: one is developing new quality productive forces, and the other is expanding domestic demand. Only by doing both of these solidly can we drive the economy to form a virtuous cycle, laying a solid foundation for the continued healthy growth of the future economy. Therefore, these two links are equally important; neither can be dispensed with.

Supply: The Evolution of Key Industries

Looking at the supply side, the process of China’s economic development over the past several decades has essentially been a process of continuous industrial upgrading and renewal. And the key question we now face is whether the next stage of industrial upgrading can be sustained and continuously advanced to higher levels.

Objectively speaking, China’s economic development has always been accompanied by innovation, but past innovation and current innovation are markedly different. Past innovation was more a matter of imitation and learning. For example, when we first developed manufacturing, many of the labor-intensive products we made were categories already matured by Japan and the Four Asian Tigers; it was only because their labor costs had risen substantially that the relevant industries gradually shifted to places like Shenzhen in China, and through following, learning, and rapid imitation, we achieved rapid industrial growth. One could say that innovation in that stage was at its core a process of learning and catching up. But now, China’s industrial development is increasingly approaching the global economic and technological frontier, and the demand for original innovation is also growing.

On whether China can continue to advance original innovation, there are differing views both internationally and domestically. I can clearly sense that the international perception of China’s innovative capacity has undergone a great change. In the past, many foreign experts dismissed China’s innovative capacity, believing China could only produce cheap products and could not deliver high-quality, innovative achievements. When speaking of Chinese innovation, the two characterizations they often cited were, first, theft of intellectual property, and second, reliance on government subsidies. But last year’s “DeepSeek moment” delivered an enormous visual and cognitive shock to many people.

An enterprise like DeepSeek neither stole others’ intellectual property nor received government subsidies, yet it developed highly competitive artificial intelligence technology and products. Looking back, there are in fact many high-quality innovative achievements domestically; not only has the international community underestimated our innovative capacity, but we ourselves often overlook it as well.

In fact, China already has quite a few emerging products that lead the world. More importantly, the current AI technological revolution offers us a rare historical opportunity, and the key going forward is to seize the opportunity and keep exerting effort, steadily advancing along the road of original innovation and driving continued breakthroughs in industrial upgrading.

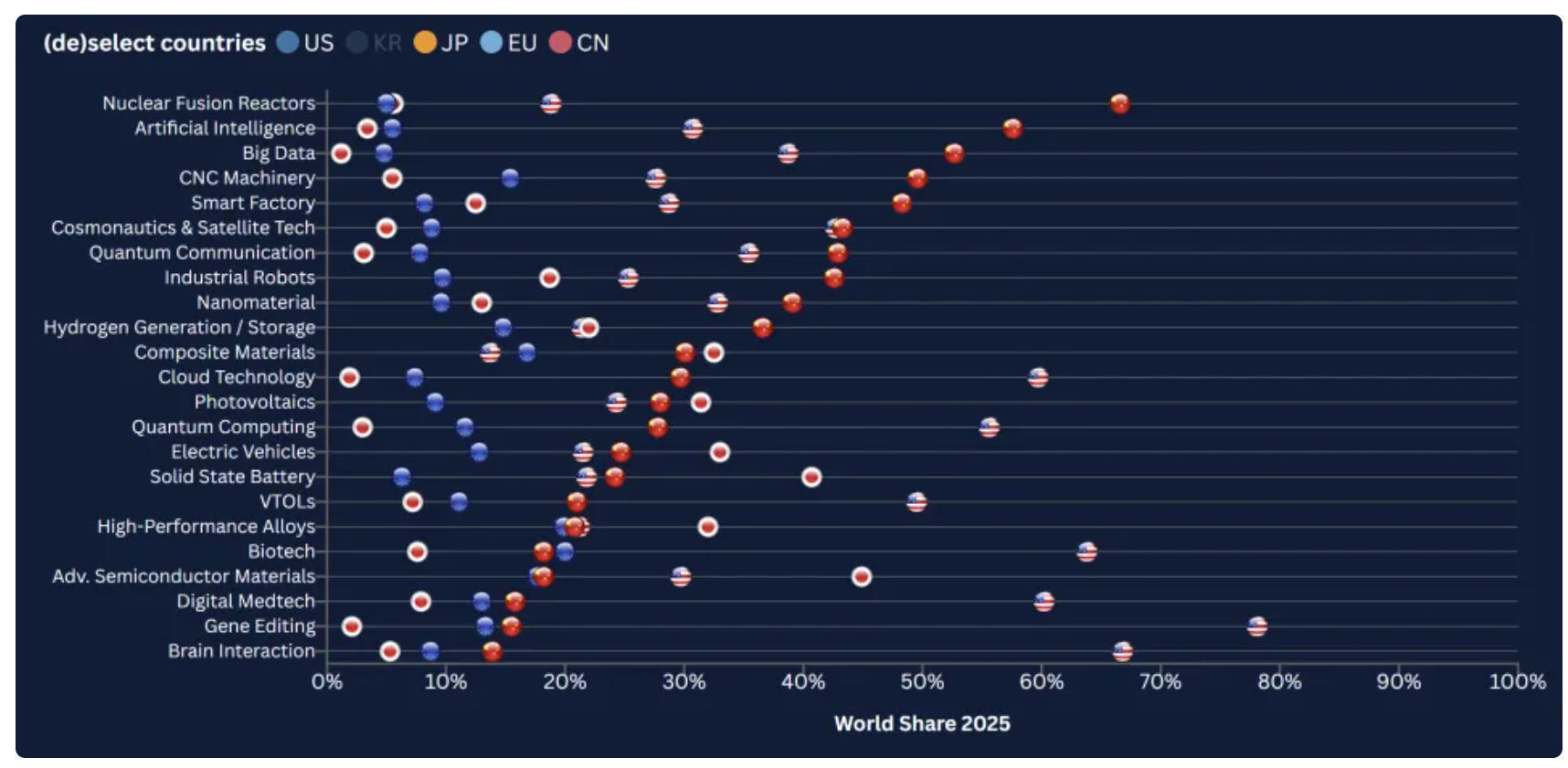

Figure 4 is the global patent market share that I downloaded from a German research institute. In the figure, the red spheres represent China, and one can see that China’s patent market share in multiple fields is already in a leading position. Of course, the United States still maintains a commanding lead in many fields, but it is undeniable that China’s relative rise is very evident.

The Opportunity of the Technological Revolution

Some believe that we still have shortcomings in original capacity for technological innovation, with our advantages reflected more at the application level. Put simply, our breakthroughs from 0 to 1 are relatively weak—especially evident against the backdrop of China-U.S. technological competition—but in industrialization and large-scale application from 1 to 100, we do quite well. As an economist, I do not regard this as a shortcoming.

NVIDIA founder Jensen Huang once said: “The country that benefits most from a technological revolution is not necessarily the one that invented the technology, but the one that can apply it quickly and well.” We do indeed have an advantage in technology application, and if we can seize this round of opportunity and take application to the extreme, we can fully drive technological progress and economic development up a major step. On that basis, we can then gradually enhance our original-innovation capacity from 0 to 1 and compete with the world’s leading countries—this may be more pragmatic.

After all, we are still a developing country, and wanting to achieve original leadership in all technological fields overnight is unrealistic. Improving core technology and original capacity is itself a gradual process of continuous accumulation. And seizing the rare current opportunity to develop the economy well is the most crucial and most urgent task for us at present.

A Solow Paradox of AI?

In the process of the spread of new technologies such as computers, the “Solow paradox” once appeared: computers were everywhere, yet no obvious improvement in productivity was reflected. With the rapid development of artificial intelligence now, many people are also questioning whether a bubble has already appeared in the AI field.

Not long ago, when I spoke with Nobel laureate in economics Michael Spence, I also asked him this question. His view is that artificial intelligence does not count as a bubble, and even if a bubble exists, it is a rational bubble. Because when a promising new technology appears, no country and no enterprise wants to be left behind, and as long as real results ultimately materialize, the upfront investment cannot be counted as waste. The internet bubble at the start of this century is a classic example: when the bubble burst, large amounts of investment seemed wasted, but the boom of that era left behind a great deal of valuable technology and also gave rise to a batch of outstanding enterprises.

In the field of artificial intelligence, my colleague Shen Yan and others have done a preliminary analysis. From macro data, artificial intelligence has not yet had a statistically significant positive boost on China’s total factor productivity; but at the micro level, whether for enterprises or industries, the improvement of efficiency and productivity from AI can already be observed in real terms.

In other words, evidence of efficiency improvement at the micro level has already appeared, only it is still at an early stage; as for when effects will show at the macro level, that remains to be seen. If we draw on the pattern of how computer technology affected productivity back then, perhaps after some more time, artificial intelligence will play a tremendous role in improving overall efficiency.

Cathie Wood, an investor focused on emerging technologies, is very optimistic about the prospect of general-purpose technologies such as artificial intelligence driving economic growth, even believing that global economic growth could reach 7% by 2030. Whether this judgment is accurate is hard to determine, but what is certain is that after general-purpose technology is deployed at scale, it could fully drive economic acceleration and significantly improve efficiency—and this is a once-in-a-lifetime opportunity for us.

Therefore, from the supply side, the outlook is on the whole optimistic; there are already many successful cases of developing new quality productive forces, as well as many promising directions.

Demand: How Consumption Can Recover

“Strong supply” still has room for improvement, and “weak demand”—especially insufficient consumption demand—is the most important contradiction at present. Will China’s future economic growth be driven by consumption or by investment? There has long been debate on this. I believe there is no need to make an absolute either-or choice; maintaining an appropriate proportion between the two may be more important for a large-country economy.

Singapore’s savings rate is very high, yet this has not affected its continued growth. China’s current-account surplus as a share of GDP fell rapidly after the financial crisis from the historical peak of 9.8% in 2007, basically stabilizing in the range of 1%–2% after 2012, and rebounding to 3.7% in 2025. Singapore’s ratio, meanwhile, has been close to 20% year after year, yet no obvious problems have emerged—the reason being that it is a highly open small-country economy whose products are exported in large quantities and absorbed by external markets. But for a large country like ours, if the gap between the shares of consumption and investment remains too large, the difficulty in the future will only grow.

Boosting consumption has become crucial at this moment, for two main reasons. First, the ultimate purpose of economic development is to meet the people’s ever-growing need for a better life. A long-standing low share of consumption shows that many needs have not been truly met. Even though we emphasize long-termism and the accumulation of capital for sustained future growth, in the end we still must improve people’s lives, so raising consumption is entirely warranted.

Second, the more urgent pressure is that if consumption fails to rise, the “strong supply, weak demand” contradiction will become even more prominent. Against the backdrop of an increasingly complex international market environment and rising uncertainty in external demand, excess capacity will become increasingly prominent. Overcapacity means declining investment efficiency and wasted resources, and economic growth then becomes hard to sustain. In this sense, boosting consumption is no longer merely a question of medium-to-long-term structural rebalancing; it may well directly bear on whether economic growth this year and next can be stabilized—a very urgent, real-world problem.

Of course, it should also be noted that China’s consumption is in fact already recovering. The lowest point of the consumption rate appeared in 2010, and it has since risen by nearly 10 percentage points—only the pace of recovery has been somewhat slow and the process relatively difficult.

Over the past two years, the government has introduced quite a few policies, such as trade-in programs, and I have enjoyed the dividend of this policy myself. My old phone had been dropped beyond recognition, so I bought a new model, originally priced at nearly 10,000 yuan; under the trade-in policy, 3,000 yuan was deducted, and the experience was quite good. But the problem is that having bought a new phone this year, I will not buy a new one again over the next two or three years, even with a subsidy. The data also bear this out: in the early period after the trade-in policy is rolled out, demand is released in a short-term burst and rebounds quickly, but after one quarter it begins to weaken, and after three or four quarters it even turns into negative growth. Essentially, this pulls forward and over-draws future demand.

Therefore, fundamentally boosting consumption ultimately comes down to two points: first, having money to spend, and second, daring to spend money. The former is an income problem, and the latter is a confidence problem. All policies aimed at promoting consumption, if they are to truly form sustainable growth, must ultimately focus their efforts on these two points. Short-term stimulus policies such as trade-in programs are not without merit, but they can hardly form long-term, stable consumption momentum.

China Online Consumer Brand Index

Let me briefly introduce a piece of research that I have carried out with collaborators. Using data from across the Taobao-Tmall network, we constructed an online consumer brand index, the purpose being to provide an observable quality indicator for online consumer products. When we shop online, the easiest thing to see is price information, but there is no indicator for product quality. Take the used-car market, for example: for two cars both driven for eight years, ordinary consumers—mostly not experts—simply cannot see the differences in intrinsic quality, which leads consumers to ultimately tend to buy only the cheapest.

The theory of the market for lemons is a classic theory in economics used to describe market failure caused by information asymmetry; the lemon market is also called the market for inferior goods (”lemon” in American slang means “an inferior product, a bad car”). Put simply, in a market where the seller knows the true quality of the goods better than the buyer, the buyer can hardly tell good from bad and can only see the price; at that point, no one dares to buy the expensive ones and only dares to buy the cheap ones, with the result that quality products cannot be sold and gradually exit the market, and ultimately all that remains is inferior products, with the entire market getting worse and worse and even shrinking.

Some platforms repeatedly emphasize “the lowest price across the network,” even promising compensation if a lower price is found elsewhere. What impact will this orientation have on the structure of product quality in the market? All manufacturers are forced to make cheap goods, because the expensive, high-quality ones cannot be sold. Of course, lowering prices can compel enterprises to improve efficiency, but efficiency improvement has its limits; once the critical point is passed, pushing prices down further can only come at the expense of product quality. This is precisely the original intention behind our research: a market cannot have only price information; it also needs reliable quality information.

The Consumer Brand Index

Based on the data, we constructed two indices, one for goods and one for cities: one is the consumer brand index, which measures the average quality level of the consumer goods purchased by consumers in a city; the other is the consumer brand purchasing-power index, which measures the overall scale of spending by that city’s consumers on consumer goods.

As can be seen, the top ten cities in brand purchasing power are Shanghai, Beijing, Hangzhou, Shenzhen, Guangzhou, Chengdu, and so on, which basically accords with common sense—the more economically developed a city, the stronger its overall consumption purchasing power naturally is. Somewhat unexpectedly, the top ten cities in the consumer brand index are Hefei, Zhengzhou, Nanjing, Nanchang, Huai’an, Hangzhou, Linyi, Huaibei, Zhoukou, and others—these are not cities as developed as Beijing, Shanghai, Guangzhou, and Shenzhen.

Our analysis found two factors that can explain this. First, the higher the share of migrant workers, the higher the brand purchasing-power index and the lower the brand index. Large numbers of migrant builders have made important contributions to urban development, but their own consumption levels are relatively low, and they mostly buy low-priced, basic-model goods. The higher this group’s share, the more it drags down the city’s overall brand index. Second, the higher the share of labor within the establishment (i.e., the public/state sector), the higher the brand index. The income of this group is not necessarily the highest, but their security is more stable and their expectations clearer, so they have money and dare to spend it.

This shows that the key to boosting consumption still lies in the two fundamental issues of income and confidence. Making the economy larger in aggregate is only one aspect; the level of social security, residents’ income expectations, and the income-distribution structure are the foundations that support sustained consumption growth.

The Ranking of Up-and-Coming Fast-Moving Consumer Goods Brands

We have also studied quite a few up-and-coming fast-moving consumer goods (FMCG) brands, which I will not go into in detail here. What I mainly want to share is that from the brand rankings, one can clearly see that the products currently doing well are mainly of two types.

One type is traditional strong brands, such as Huawei and Apple, which still enjoy strong market acceptance even with relatively high pricing, because brand information is transparent and consumers have clear expectations of quality.

The other type that performs outstandingly is what we call up-and-coming FMCG brands, many of which come from emerging niches—such as baby sunscreen, pet products, and beauty cosmetics. Many of these subcategories were previously unfamiliar to the general public and even beyond many people’s imagination, yet they are all developing very well now.

What is even more interesting is that the manufacturing and supply-side innovation mentioned earlier is reflected especially prominently in the consumer goods sector. Of these successful up-and-coming FMCG brands today, more than 90% are domestic brands rather than international brands. And these domestic brands are priced no lower than international brands—some are even more expensive—yet they are still accepted by the market. This also shows that our innovation is diverse and rich, reflected not only in industries such as artificial intelligence, digital technology, and green energy, but equally in the consumer goods sector, where the deep integration of digital technology with market demand has given rise to a large number of entirely new products and niches.

The Future Direction of the Economy

The future direction of the economy is very clear, and the most important thing is “dual circulation.”

Among these, industrial upgrading and renewal is key. Over the past dozen or so years, our economic growth has continuously faced downward pressure, partly because industrial upgrading and renewal has not advanced smoothly enough. On the one hand, industries that have lost competitiveness and should have exited have not been cleared in a timely manner, and the overcapacity problems of many traditional industries remain prominent to this day; on the other hand, the scale and supporting strength of emerging industries are still clearly insufficient. Although emerging industries have developed rapidly in some fields, new problems have also arisen from everyone rushing in and expanding too fast.

Overall, industrial upgrading and renewal is both a huge challenge we currently face and a source of abundant opportunities. In my conversations with friends in the venture capital industry, they generally believe that another golden age of innovation and entrepreneurship has now arrived. When a general-purpose technological revolution arrives, the entire economic structure and business models may be redefined, and with that come a great many new opportunities.

These include opportunities brought by the rise of consumption demand in the process of domestic economic rebalancing, as well as opportunities to create new demand through supply-side innovation—many consumers originally did not know such products existed, but once good supply-side innovation appears, it quickly opens up the market.

From a macro perspective, we do indeed face enormous challenges, and economic transformation is by no means easy; but if we look at the micro level, we may well be standing at a new inflection point for a breakout, about to enter a period when opportunities for innovation and entrepreneurship emerge in concentrated form.

A Policy Combination

The current slowdown in economic growth is not simply a cyclical problem; it is not like responding to the Asian financial crisis in the past, where strong macro policy underpinned the economy and it could smoothly come out. The situation this time is not so simple and requires a policy combination, comprising five aspects: macro policy, market-oriented reform, balance-sheet restructuring, “investing in people,” and the international economic order.

1. Macroeconomic Policy

With the economy facing downward pressure, it is only natural for macro policy to exert force at the appropriate time, and I believe this year’s fiscal and monetary policy will have new arrangements. The difficulty is that macro policy must both stabilize growth and effectively ease the “strong supply, weak demand” contradiction—and if handled improperly, it may instead aggravate this contradiction. Because we have been better at stimulating supply in the past and not good at directly driving consumption, this is indeed a tough problem for decision-makers. Once stimulus is applied, funds easily flow into investment and production, making supply even stronger and demand relatively even weaker in the next stage; but the paths and levers for directly and effectively stimulating consumption are not clear.

Many experts believe that fiscal policy should play a more important role in this round of macro-control, because fiscal policy can more precisely reach sectors, industries, and specific fields, exerting force more directly. Of course, while increasing fiscal support, it is also necessary to balance the supply-demand structure—funds cannot be deployed only into infrastructure and industrial parks, or it will only make the “strong supply, weak demand” problem more prominent.

Monetary policy must likewise play a role, with the focus placed on effectively boosting demand. In these years the central bank has also been using and adjusting various structural monetary policy tools; the relevant measures must be precisely implemented to truly take effect, and the aggregate and proportions must be well managed—they cannot be overused, because monetary policy is essentially an aggregate policy. For example, now that “investing in people” is emphasized, could the central bank consider setting up a special re-lending facility for “investing in people”? If it could be genuinely implemented, the effect should be good.

Overall, macro policy must provide support for economic growth, but it may not be the most important role in this round of adjustment. When some countries roll out powerful macro policies, it is usually when the economy faces a serious crisis. Although we currently face downward pressure, we are still far from the stage where strong stimulus is needed.

2. Market-Oriented Reform

Even more crucial is to continuously advance market-oriented reform, allowing the market mechanism to truly play a decisive role in resource allocation—this is also the reform direction made clear at the Third Plenary Session of the 20th Central Committee. This reform is crucial to both the supply and demand ends.

From the supply side, having the market allocate resources means that investment and capacity decisions must follow market signals. The “involution” (neijuan) problem that has been hotly discussed in the past two years has complex causes, but we must be especially vigilant about local governments’ non-standard investment-attraction behavior. Such behavior easily deviates from market demand and expands capacity blindly; it fails to effectively raise technological levels and instead rapidly amplifies capacity, intensifying overcapacity pressure and depressing investment returns. Insisting that the market decide what to invest in and how much, while regulating industrial policy and restricting and clearing up non-compliant and illegal industrial subsidies, is precisely the clear governance direction at present.

From the demand side, deepening market-oriented reform helps market entities and the household sector obtain more income. For example, the land-transfer revenue obtained by localities is often concentrated by the government into large projects in pursuit of immediate GDP effects—equivalent to using all of it for investment, with a savings rate of 100%. If more public resources were directed toward people’s livelihoods rather than all concentrated on construction, residents’ consumption rate would naturally rise accordingly. Raising household income, improving public welfare, and having resources allocated more by the market, enterprises, and residents is more conducive to boosting consumption and to a virtuous economic cycle than allocation led solely by the government.

While advancing market-oriented reform, the public policy system must also be further innovated and improved. We currently have two core tasks—developing new quality productive forces and expanding domestic demand—and here lies a risk to be wary of: that new quality productive forces develop too fast while employment support fails to keep up, possibly further intensifying the “strong supply, weak demand” contradiction. For example, if artificial intelligence is deployed at scale and factory employment is greatly reduced, with residents’ wage income and job opportunities declining, where will consumption come from?

I once spoke with former U.S. Treasury Secretary Robert Rubin, who mentioned the employment plight of blue-collar youth in small American towns; China may face similar challenges in the future. As an optimistic economist, I believe technology destroys old occupations and also creates new ones. But Professor Jiang Xiaojuan’s observation has deeply inspired me: since the 1980s, the jobs and employment opportunities destroyed by technological innovation have exceeded the newly created positions, and the economy’s overall employment density has been declining.

Even as high-end industries flourish, the ordinary workers who are replaced find it very hard to transition smoothly. This poses a stern demand on public policy. Our technological innovation should adhere to an employment-priority orientation; technology should serve people, not simply replace them. There is nothing wrong with entrepreneurs pursuing efficiency, but the government needs to design new policy frameworks and tools to ensure that, throughout the process of technological progress and structural transformation, the people always have money to spend and dare to spend it.

3. Balance-Sheet Restructuring

The adjustment of the real estate market has already placed clear pressure on the balance sheets of households, local governments, and financial institutions, which has to a certain extent directly suppressed domestic demand, especially consumption demand. In this situation, consideration can be given to having the central government moderately add leverage to help various micro entities repair their balance sheets.

Although the central government also has some implicit debt, its overall debt ratio is relatively low, whereas local governments face heavy debt pressure, much of which is not directly reflected on the central government’s balance sheet. Local governments cannot go bankrupt, and once they encounter payment difficulties, the ultimate responsibility must still be borne at the central level. Therefore, through a round of systematic asset restructuring, the central government can moderately expand leverage to ease the balance-sheet pressure on other economic entities, creating conditions for economic recovery. This is exactly what the United States did during the global financial crisis. If large numbers of our economic entities continue to be troubled by debt burdens and shrinking assets, both domestic demand and investment will be severely suppressed, and the economy will find it hard to truly stabilize and rebound.

In addition, the balance sheet of the social security system is not very healthy either. At present, the social security fund as a whole still has a large funding gap, especially for the groups of rural migrant workers, migrant laborers, and rural residents, whose level of protection is on the low side and whose gap is more prominent. Although policy has been gradually improving in recent years, the magnitude of the annual increase is still on the small side. I believe consideration can be given to transferring state-owned assets more vigorously to replenish the social security fund and to carry out a more forceful structural adjustment of the social security system, genuinely strengthening residents’ level of protection and confidence to consume.

4. The “Investing in People” Policy

“Investing in people” is a direction that has been emphasized in recent years and is worth promoting with great effort. The fundamental purpose of economic development is to let the people live better.

“Investing in people” means improving the safeguards for people’s livelihoods across the full life cycle, including raising the quality of education, improving medical services, and refining the social security system, so as to enhance people’s sense of happiness and gain. At the same time, “investing in people” is also about accumulating human capital—by raising the quality of workers and supporting employment and entrepreneurship—to provide solid support for developing new quality productive forces.

In the future, whether local governments, various institutions, or society at large, all should shift their investment focus more from the traditional “investing in things” toward “investing in people.” This is conducive both to expanding domestic demand and improving livelihoods, and to effectively raising total factor productivity.

5. A Responsible Major Country

As a large country, the external environment and international rules we face are undergoing profound change, and we must participate in global economic governance in a responsible posture.

In recent years, discussions of international economic and trade rules have become increasingly intense, with some developed countries continuously questioning China’s status as a developing country within multilateral frameworks. In 2024, the U.S. Congress passed relevant legislation arguing that China should no longer be allowed to enjoy special and differential treatment as a developing country, contending that China’s economic scale no longer fits the relevant arrangements. In response, Premier Li Qiang announced at the UN General Assembly in September 2025 that China, as a responsible major developing country, will not seek new special and differential treatment in current and future World Trade Organization (WTO) negotiations. This important statement clearly demonstrates our sincerity and willingness to take the initiative in shouldering the responsibilities of a major country and to adapt to the transformation of global governance.

In the future, how to grow together with global economic partners for mutual benefit will be a major proposition we face. If we remain stuck in the traditional mindset of “my products are high-quality and low-priced and should rightly occupy the market,” our room for development will only narrow. Today many countries pay more attention to industrial security and structural adjustment, and pure advantages in price and quality are no longer sufficient to dispel external concerns.

In this regard, we are also actively exploring new paths. The Institute of South-South Cooperation and Development, established under the National School of Development at Peking University, is an important platform that General Secretary Xi Jinping advocated in 2015 and that was formally established in 2016. On the one hand, it distills pragmatic and feasible policy experience from China’s development practice, striving to form a “Global South consensus” suited to the broad range of developing countries; on the other hand, it seeks new approaches for enterprises going abroad, encouraging enterprises to deeply integrate into local economies—producing locally, creating jobs, and contributing tax revenue—thereby easing domestic capacity pressure while achieving an integration of interests with host countries.

A few years ago I proposed the idea of a “Global South Green Development Plan.” China’s green energy industry has significant advantages but also faces the pressures of overcapacity and trade barriers, while many developing countries urgently need green products to support their energy transitions. This is like America’s “Marshall Plan” of the past, which, through financial and industrial support, helped Europe revive—and the ultimate biggest beneficiary was in fact the United States, which both consolidated its alliance system and propelled the dollar onto the global stage. Such win-win cooperation is worth our careful planning.

From a domestic perspective, even if the “strong supply, weak demand” contradiction is hard to thoroughly resolve in the short term, as long as we continuously optimize the external environment and strengthen international cooperation, we still possess broad room for growth. In cooperating with many developing countries, competitive conflict is relatively mild—for example, our new-energy vehicles encounter resistance in some markets, but new-energy motorcycles are very popular in many African countries, where power infrastructure is weak, and we set up photovoltaic panels for them, solving the energy-supply problem. Overall, there is still much room for international cooperation. China’s economic development today is no longer simply about exporting products outward, but about growing together hand in hand with partner countries—this is the path of long-term sustainable development.

More to read:

Professor Huang Yiping directly interprets China’s low household consumption share of GDP as evidence of insufficient household consumption, and then explains that “consumption insufficiency” as a problem of inadequate income and social security. This skips over the most important issues in China’s case: wealth structure, asset structure, and stage of development.

First, China’s actual volume of household final consumption is already among the highest among countries at a similar income level. In many Chinese cities, household consumption of physical goods, durable goods, restaurants, tourism, electronics, and automobiles is already close to, and in some areas above, that of lower- and middle-income households in many advanced economies. I made this point in my earlier essay, China’s Vastly Underestimated Consumption Volume.

Second, “anxiety about healthcare, retirement, and unemployment” cannot fully explain China’s high household savings rate. Households in every country worry about these issues. Americans worry even more about medical bills. Europeans worry about unemployment and pension sustainability. Japanese households worry about aging. As I argued in How China’s Housing and Education “Funding Cycles” Suppress Consumption, the more specific mechanism behind China’s elevated household savings is housing down payments, mortgage pressure, children’s education costs, marriage and childbirth costs, urban settlement costs, and the expense of maintaining one’s class position. This is not merely an abstract lack of security. It is a long-term funding pressure created by asset prices and intergenerational competition.

Third, the deeper macroeconomic root is the relatively low household share of national wealth. If Chinese households directly hold only about half of national wealth, while American households hold a much higher share, then China’s household income share and household consumption share will naturally be lower. This cannot be solved simply by issuing consumption vouchers, raising wages, or expanding social security. It involves the land system, state-owned assets, local government finance, the financial system, corporate retained earnings, government investment mechanisms, and China’s system of integrated mixed ownership.

Fourth, however, the issue must also be understood dialectically. Precisely because China has a mixed-ownership structure, with the government and state-owned enterprises holding a large share of national wealth, state-owned enterprises can undertake massive infrastructure and public-service investments that private capital would not or could not bear. Chinese households therefore indirectly enjoy a level of public welfare and basic services that is relatively advanced among major economies. These benefits are not fully captured in measured household consumption.

Chinese households may not directly hold as large a share of national wealth, but a significant portion of that wealth has not simply been “wasted” or “taken away.” It has been embedded in the state, SOEs, land, infrastructure, utilities, and industrial-capital systems. It flows back to households in other forms: high-speed rail, subways, ports, power grids, telecommunications networks, public safety, logistics, low-cost public services, urban infrastructure, industrial employment, and supply-chain efficiency.

Therefore, China’s low consumption share of GDP does not automatically mean that Chinese households have low welfare. Many forms of welfare do not appear as household cash income or final consumption. They exist as public capital stock, quasi-public services, low-cost infrastructure, and state organizational capacity.

This is the biggest blind spot in Huang Yiping’s consumptionist framework. It only sees the visible income and visible consumption of the household sector. It does not see the implicit welfare provided by China’s public capital and state-owned capital system.

What is more worrying is that even a senior policy intellectual such as Professor Huang seems to have accepted the consumption-stimulus framework and the idea that the root cause of global trade imbalances lies in China’s insufficient consumption.

This easily pushes China into both a Western narrative trap and a strategic trap: stimulate consumption, restrain investment, and control “overcapacity” in the name of restoring global balance. In practice, that would amount to voluntarily weakening China’s own economic strengths.

China does not have a general overcapacity problem. Its overall capacity-utilization rate is roughly in the middle range among the world’s 50 largest economies. China does not have an investment-excess problem either. In per-capita infrastructure stock, China still has a substantial gap with Europe, the United States, and Japan. Nor does China have a real consumption-insufficiency problem. China’s per-capita consumption volume is already among the highest in the world for its income level — something many Chinese people can sense from everyday experience.