Miao Yanliang: China Should Advance Capital-Account Opening to Support RMB Internationalization

CICC chief strategist urges China to advance currency internationalization through greater exchange-rate flexibility, deeper onshore and offshore markets, and a stronger RMB cycle.

I’ve seen an increasing number of Chinese economists talking about RMB internationalization recently. So for today’s episode, I decided to introduce an article by Miao Yanliang缪延亮, Director and Chief Strategist at China International Capital Corporation (CICC). Miao earned a Bachelor of Engineering from Shanghai University in 2001, a Master’s degree in Economics from Fudan University in 2004, and a Ph.D. in Economics together with a Master’s in Public Policy from Princeton University in 2008. He joined the IMF in 2008, where he worked successively in departments covering emerging markets and debt policy, and was involved in the response to the European sovereign debt crisis.

After returning to China in 2013, Miao served at the State Administration of Foreign Exchange (SAFE) for a decade. From 2013 to 2018, he served as Senior Advisor to the Administrator of SAFE and as Head of Research at the SAFE Investment Center, where he led global macro and strategy research related to the management of foreign exchange reserves. In May 2018, he was appointed Chief Economist of the SAFE Investment Center. In 2023, Miao joined CICC. In July 2024, he attended an expert symposium on the economic situation chaired by Premier Li Qiang.

The article takes the United States’ “countercyclical opening” of its capital account in 1974 as a case study, revisiting how—at a moment of damaged credibility and stagflation following the collapse of the Bretton Woods system—the U.S. managed to rebuild the “dollar recycling” mechanism and consolidate the dollar’s status as the global reserve currency precisely by opening up. But I believe the author also intends to offer policy recommendations for RMB internationalization.

Miao argues that China should move beyond the static mindset that equates opening up with increased risk exposure and instead adopt a dynamic perspective on trade-offs. He believes that, in the short term, capital account liberalization may indeed bring a period of pain brought by capital outflows and exchange rate volatility, similar to what the United States experienced between 1974 and 1982. Yet so long as a sustainable “outflow–inflow” cycle can be established through institutional arrangements such as greater exchange rate flexibility, the coordinated development of onshore and offshore markets, and the expansion of RMB-denominated invoicing and settlement networks, opening up will, through the very dynamics of two-way capital flows, drive market pricing mechanisms, hedging instruments, and the macroprudential framework toward greater maturity, which ultimately strengthening the resilience of China’s financial system against external shocks. Prolonged closure, the author contends, carries its own costs: if RMB-denominated assets cannot be conveniently held and allocated by overseas entities, the RMB will struggle to evolve from a settlement currency into an investment and reserve currency.

The Chinese version can be found on the webpage of the CF40 Forum. Thanks to Dr.Miao’s kind authorization, I can publish the English version in my newsletter.

How the United States Opened Its Capital Account Against the Tide

The United States today is often viewed as a symbol of free capital flows and financial openness. Yet what is little known is that the complete opening of its capital account did not happen overnight. Rather, it is a history of dynamic trade-offs centered on the interests of reserve-currency status, balancing the benefits of dollar hegemony against the risks to financial stability.

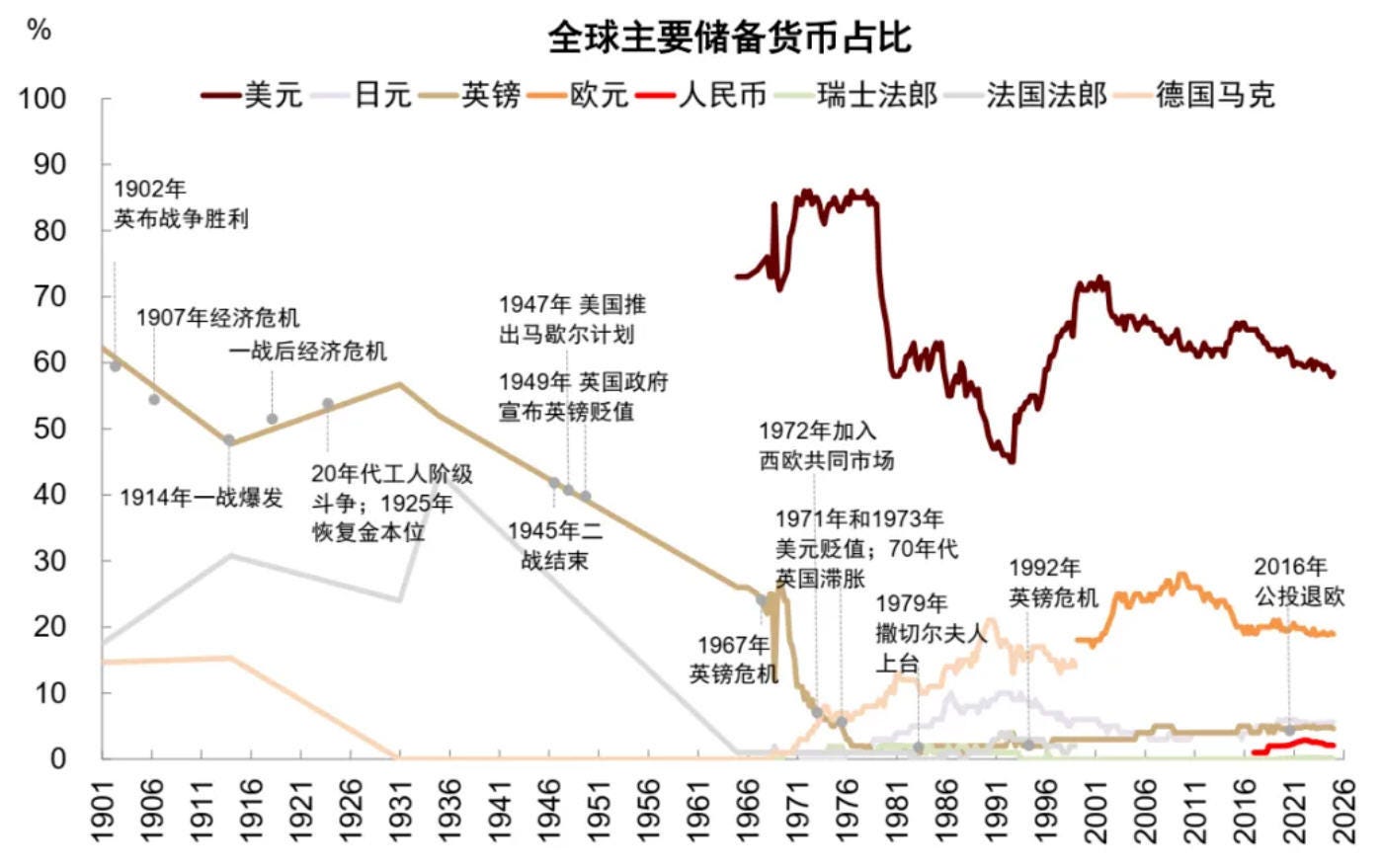

From the late 19th century to the eve of World War I, the United States was broadly part of an open system under the gold standard, but international financial centers were still dominated by London, and the dollar’s international financial functions were limited. It was only after the establishment of the Federal Reserve in 1913 that the United States, by institutionalizing the Banker’s Acceptance market and providing discount support, propelled the dollar toward internationalization.

During the Great Depression and World War II, in order to maintain financial stability and the security of gold reserves, the United States imposed controls on gold and capital flows. After World War II, the Bretton Woods system established the dollar’s status as the central currency, but it also saddled the dollar with the rigid commitment of being pegged to gold.

In the 1960s, as the U.S. balance of payments deteriorated and pressure from gold outflows intensified, the United States—in order to maintain fixed exchange rates and the dollar’s reserve-currency status—was forced to introduce a series of capital control measures such as the Interest Equalization Tax and restrictions on foreign credit.

However, entering the 1970s, capital account controls did not truly prevent the arrival of the dollar crisis; instead, they gradually came to threaten the dollar’s reserve-currency status. As global trade and cross-border capital expanded rapidly, the irreconcilable contradiction between fixed exchange rates and cross-border capital flows continued to intensify. In 1971, the Nixon administration was forced to announce the closing of the gold window, the Bretton Woods system moved toward collapse, the dollar depreciated sharply against major currencies, and the dollar’s credibility suffered a severe blow.

At the same time, the increasingly powerful offshore dollar market gradually weakened the effectiveness of U.S. onshore controls, and after the oil crisis, the massive dollar surpluses of oil-producing countries also needed a sufficiently open and deep financial market to absorb them. At this point, if the United States clung to capital controls, it might not truly prevent dollar outflows, but could instead weaken the position of the New York financial center and forfeit the reserve-currency dividend.

To consolidate the dollar’s reserve-currency status, amid the adversity of shaken dollar credibility, high global inflation, and a U.S. economy mired in stagflation and recession, in 1974 the United States instead chose to loosen restrictions on capital flows and promote the opening of the capital account.

In hindsight, this “opening against the tide” was indeed accompanied by net capital outflows and dollar depreciation in the short term, but over the long run it became the starting point for the dollar system to move from crisis toward strengthening. In the decade that followed, the United States absorbed global surplus funds through petrodollar recycling, restored price stability and reshaped dollar credibility during the Volcker era, and unleashed growth momentum with the supply-side economics of the Reagan administration—gradually forming a dollar cycle that allowed the dollar system to complete a restructuring from crisis to reinforcement.

So why did loosening capital controls at a moment of dollar fragility ultimately not weaken the dollar system, but instead become the starting point for its renewed strengthening? Was this choice a proactive plan by the United States to reshape the dollar cycle, or a passive adjustment forced by crisis?

More importantly, today—when dollar credibility is once again being questioned and the global monetary system is fragmenting at an accelerating pace—what lessons does the U.S. experience hold for the current internationalization of the renminbi and for high-level capital-account opening? This article will analyze the questions above.

I. How to Open? Under the Twin Crises of Dollar Credibility and the U.S. Economy, Rebuilding the “Dollar Cycle” Through Openness to Consolidate Reserve-Currency Status

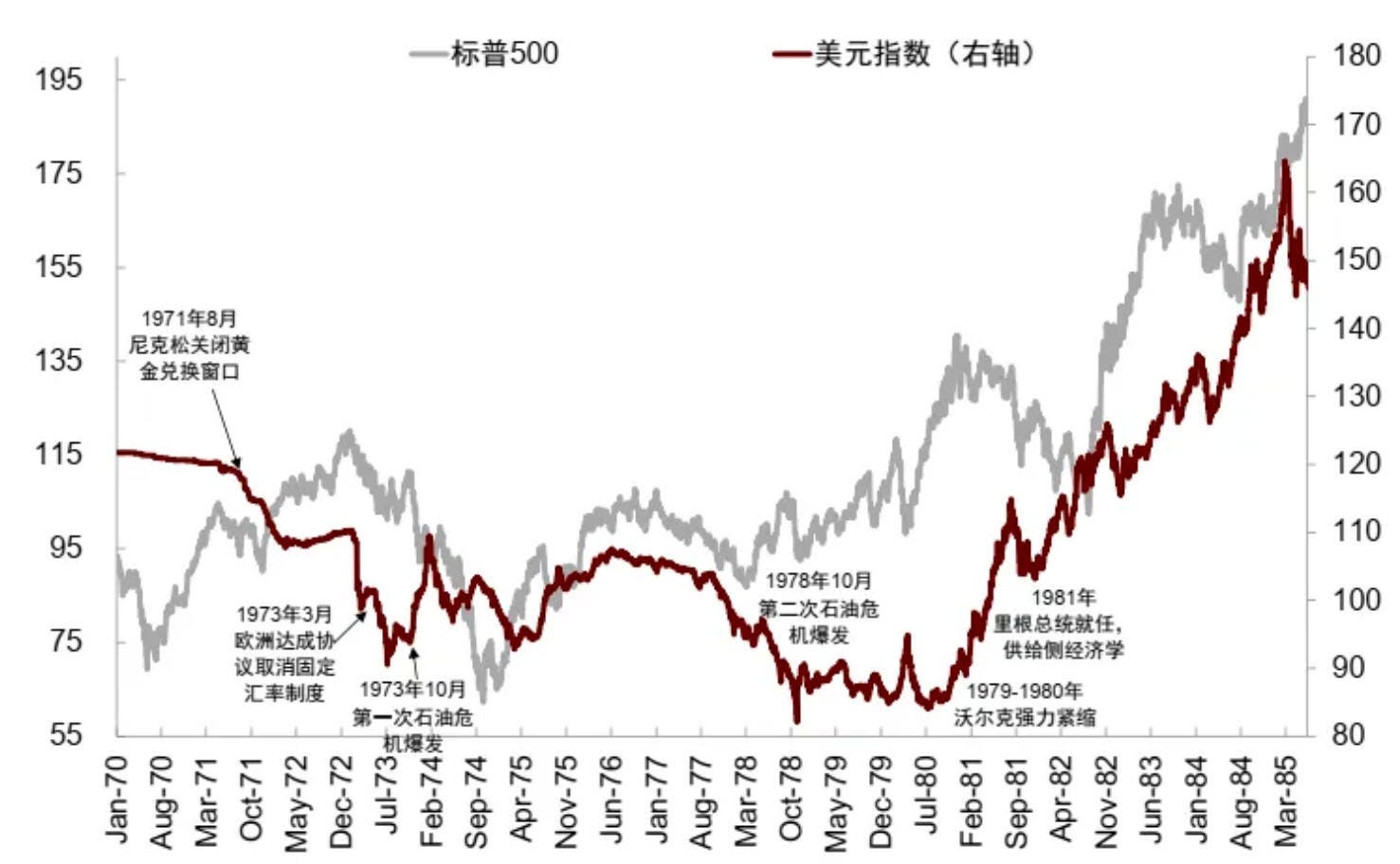

In the early 1970s, the United States faced a critical turning point for dollar credibility following the collapse of the Bretton Woods system. In August 1971, with international capital flowing at an accelerating pace and the dollar–gold convertibility commitment becoming unsustainable, then-President Nixon announced the closing of the gold window, decoupling the dollar from gold and leaving the Bretton Woods system in name only.

In less than a year that followed, the dollar depreciated markedly against the currencies of major developed economies, and the dollar’s share of global reserves—which had reached a peak of 85% in the fourth quarter of 1970—fell rapidly. In March 1973, the dollar depreciated again, but this failed to stabilize market confidence; a large-scale dollar sell-off emerged in international foreign exchange markets, major European currencies were forced to shift to floating exchange rates, and the Bretton Woods system collapsed completely.

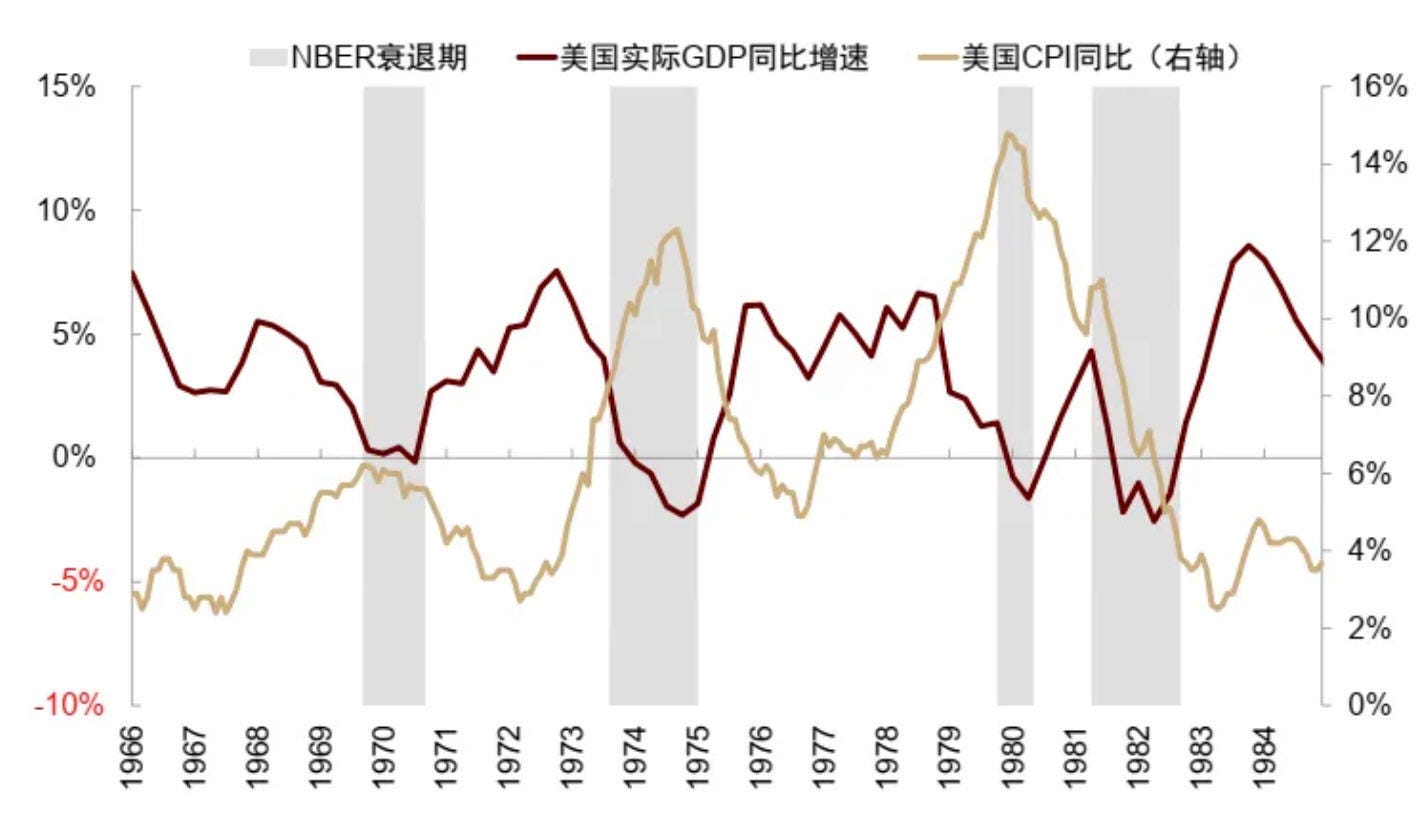

Just as dollar credibility fell into difficulty, the first oil crisis further amplified U.S. macroeconomic pressures—yet it also unexpectedly opened a window for rebuilding the dollar cycle.

In October 1973, the Fourth Middle East War broke out, OPEC announced an oil embargo, and the first oil crisis erupted in full. The rapid rise in oil prices, on the one hand, brought pressure to the U.S. economy—the U.S. economy fell into stagflation and ultimately entered recession in the fourth quarter of 1973. On the other hand, it also caused OPEC countries to accumulate large dollar surpluses, while U.S. financial markets—especially the Treasury market—possessed asset capacity and liquidity advantages rare in the world.

At the same time, the rise in oil prices also created demand for dollar payments. Combined with the fact that the oil crisis hit economies heavily dependent on Middle Eastern oil—such as Europe and Japan—even harder, these factors together pushed the dollar index from 94 before the first oil crisis to 109 in January 1974, briefly “steadying” a dollar that had been depreciating successively since the collapse of Bretton Woods.

At this point the United States faced a dilemma over whether to open its capital account: the United States urgently needed Middle Eastern petrodollar funds to flow back into the Treasury market, in order to consolidate demand for dollar assets and provide financing support for a U.S. economy in recession. At the same time, as cross-border capital flows became increasingly frequent, exchange rates turned to floating, and the offshore dollar market developed, capital controls became increasingly difficult to maintain (Hawley, 1987).

But the problem was that opening the capital account amid economic recession and a shaken dollar position could also amplify pressures from capital outflows and dollar depreciation. Facing this trade-off, Paul Volcker wrote in his memoirs that, in the context of 1974, opening the capital account to allow foreign funds into New York’s capital markets was more advantageous (Volcker & Gyohten, 1992).

In January 1974, the United States chose to open its capital account amid economic recession. Specific measures included:

Abolishing the Interest Equalization Tax (IET) established in the 1960s to prevent capital outflows, so that U.S. investors purchasing foreign securities would no longer be taxed.

Abolishing Balance of Payments Controls and loosening restrictions on outward foreign direct investment (OFDI) by U.S. residents.

Abolishing the Voluntary Foreign Credit Restraint (VFCR) and other limits on the amount of overseas lending by banks.

Subsequently, in the 1980s the United States gradually relaxed “Regulation Q,” which capped bank deposit interest rates, and formally abolished the relevant arrangements in 1986, while also establishing International Banking Facilities (IBFs)—moving toward financial deregulation and further embracing offshore markets.

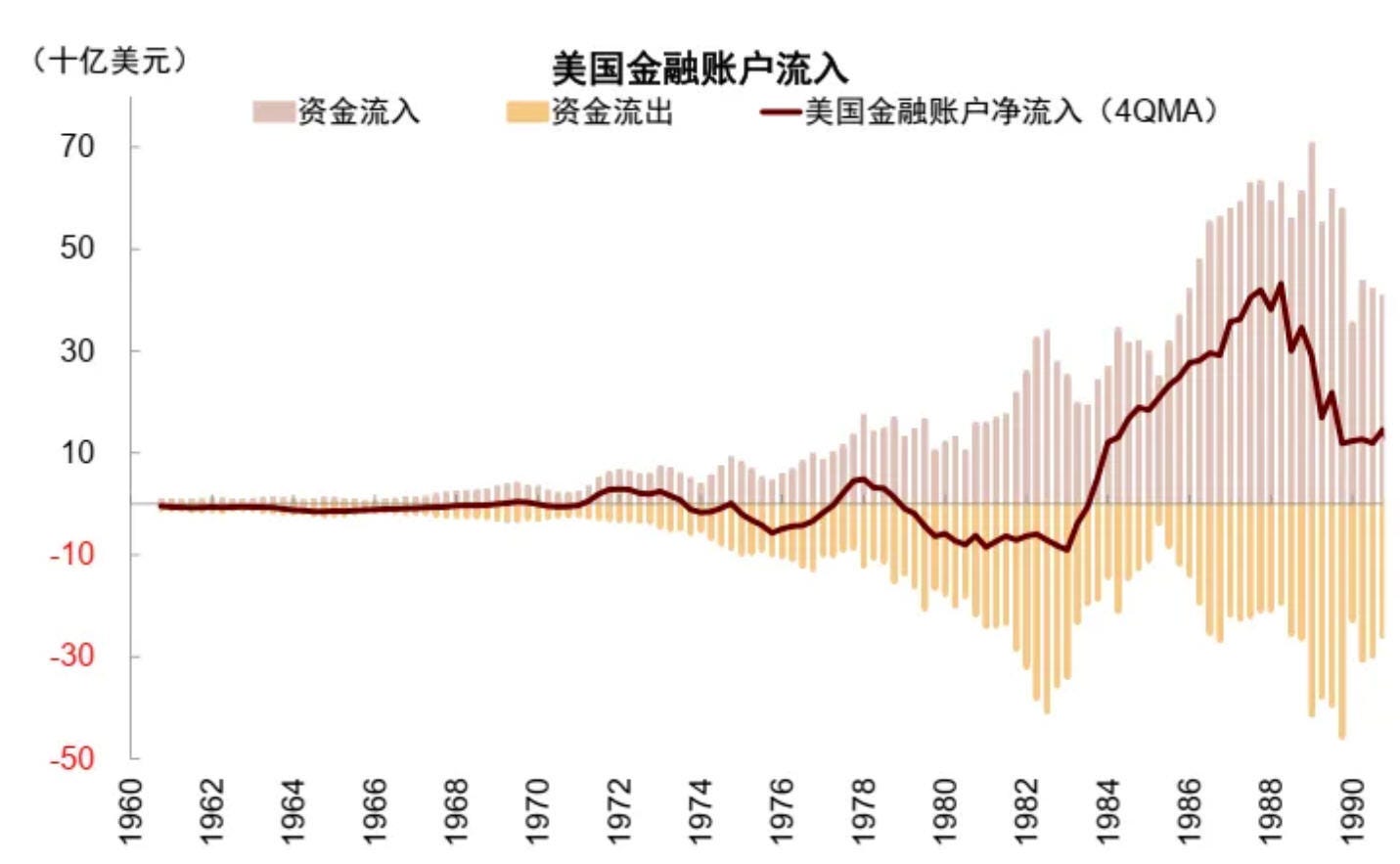

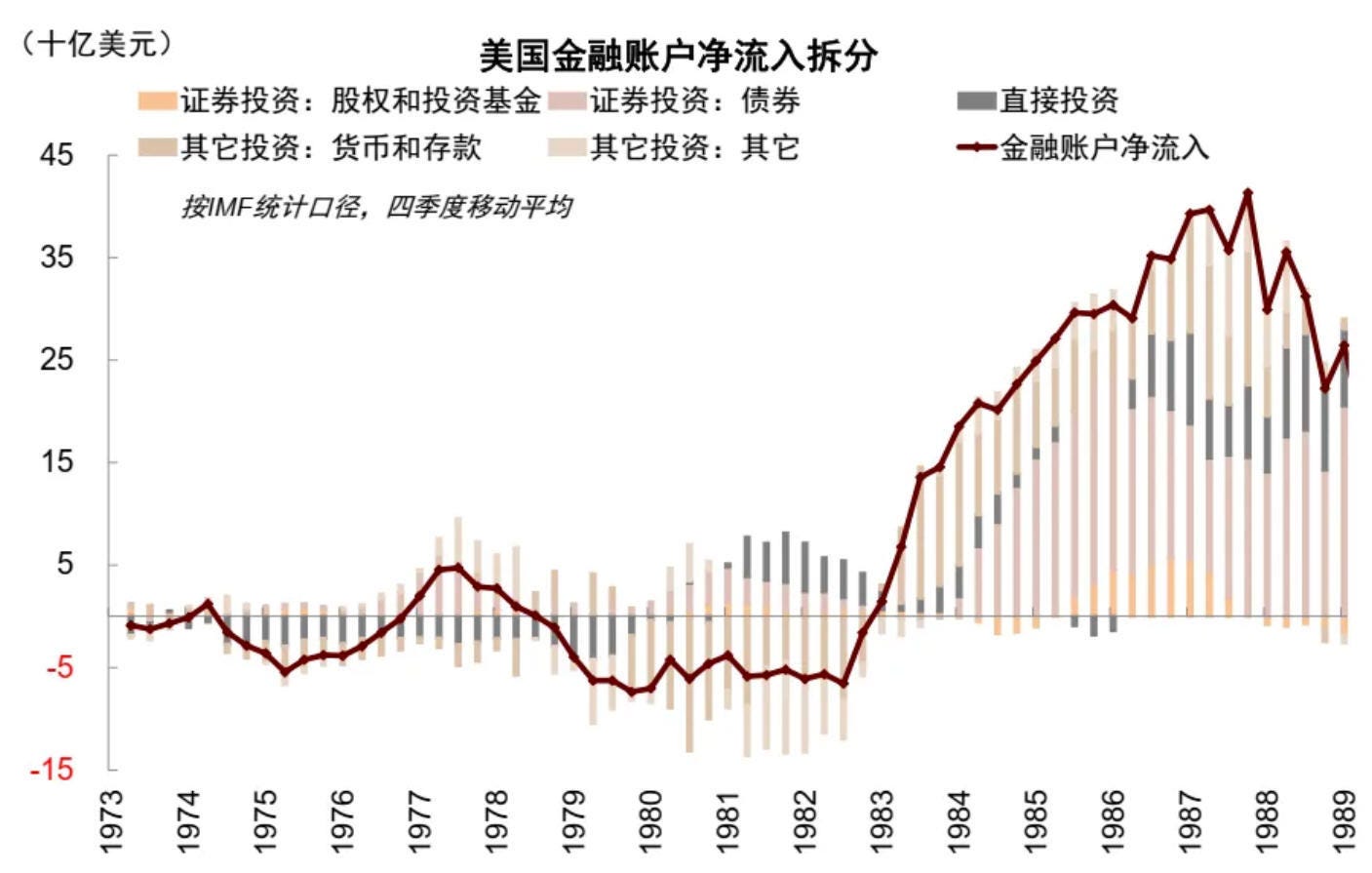

In the early stage of capital-account opening, the United States did indeed experience a “painful period” of economic recession, capital outflows, and dollar depreciation. After opening the capital account in January 1974, the U.S. economy remained in recession. It was not until March 1975 that it bottomed out and stabilized.

In the early stage of opening the capital account, the United States did indeed see net capital outflows. Although in mid-1974 the United States signed a petrodollar agreement with Saudi Arabia, stipulating that Saudi Arabia would invest part of its oil revenue in Treasuries—boosting inflows under the portfolio investment item of the U.S. financial account—the simultaneous expansion of overseas lending by U.S. banks led to outflows under the other investment item.

The result was that from 1974 to 1982, the U.S. financial account overall still showed net outflows abroad, briefly turning to net inflows only from 1977 to 1979. The economic downturn and capital outflows reinforced each other, pushing the dollar index down from its peak of 109 in January 1974 to a low of 82 in October 1978—a 25% depreciation in less than five years.

But over a longer horizon, opening the capital account did not weaken the dollar system; instead, it became a necessary condition for rebuilding the “dollar cycle” and re-steadying dollar hegemony. The key was not whether capital flowed back immediately after opening, but that the United States provided global dollar funds with a financial market that could be entered, settled into, and allocated.

It was precisely under the combined effects of petrodollar reflux after capital-account opening, the repair of dollar credibility, and steady U.S. growth that the United States, from the late 1970s through the 1980s, gradually completed the restructuring of the dollar system from crisis-induced pressure to a strengthened cycle.

► The petrodollar mechanism promoted dollar reflux: In July 1974, then-Treasury Secretary William E. Simon traveled to Saudi Arabia and reached a secret agreement. Although the dollar had already dominated the pricing of international oil trade before the petrodollar mechanism formally took effect, the agreement further consolidated and institutionalized the dollar’s dominant position as the currency for pricing and settling oil.

More importantly, Saudi Arabia committed to investing part of its dollar revenue from oil exports in U.S. Treasuries, thereby forming an important reflux mechanism for the dollar cycle. In exchange, the United States provided military protection to Saudi Arabia, and the U.S. Treasury provided Saudi Arabia with an “Add-ons” special window for Treasuries, allowing Saudi Arabia to purchase Treasuries directly, bypassing open competitive bidding.

► In the 1980s, Volcker restored price stability and reshaped dollar credibility, while the Reagan administration’s supply-side economics stimulated growth, forming a positive feedback loop: In 1979, Paul Volcker became Chairman of the Federal Reserve, placing inflation control at the core of policy and stabilizing prices through tough tightening—even at the risk of triggering recession—to revive market confidence in the dollar. The federal funds rate at one point rose above 20% in the early 1980s; high interest rates suppressed U.S. inflation and rebuilt the dollar’s purchasing power, with the year-over-year U.S. CPI falling from 14.8% in March 1980 to 2.5% in July 1983.

The process of monetary tightening came at a high cost: the United States fell into recession twice, in February 1980 and August 1981, but it also raised the real returns on dollar assets, attracting global funds into U.S. bond and deposit markets and laying the foundation for rebuilding dollar credibility.

In 1981, Ronald Reagan became President of the United States, and facing economic recession he adopted supply-side propositions to stimulate growth, spurring investment and supply recovery through tax cuts, accelerated depreciation, deregulation, and other measures. Although the goal of “small government” was not truly achieved—the U.S. fiscal deficit ratio (monthly average of -4.1%) actually expanded compared with the 1970s (monthly average of -1.9%)—fiscal expansion, tax incentives, and financial liberalization together boosted U.S. economic growth.

U.S. real GDP growth, after touching a low of -2.6% in the third quarter of 1982, entered a nearly two-year upward channel, reaching a peak of 8.6% in the first quarter of 1984. The dollar also rose sharply from its low of 85 in 1980 to a peak of 165 before the 1985 Plaza Accord.

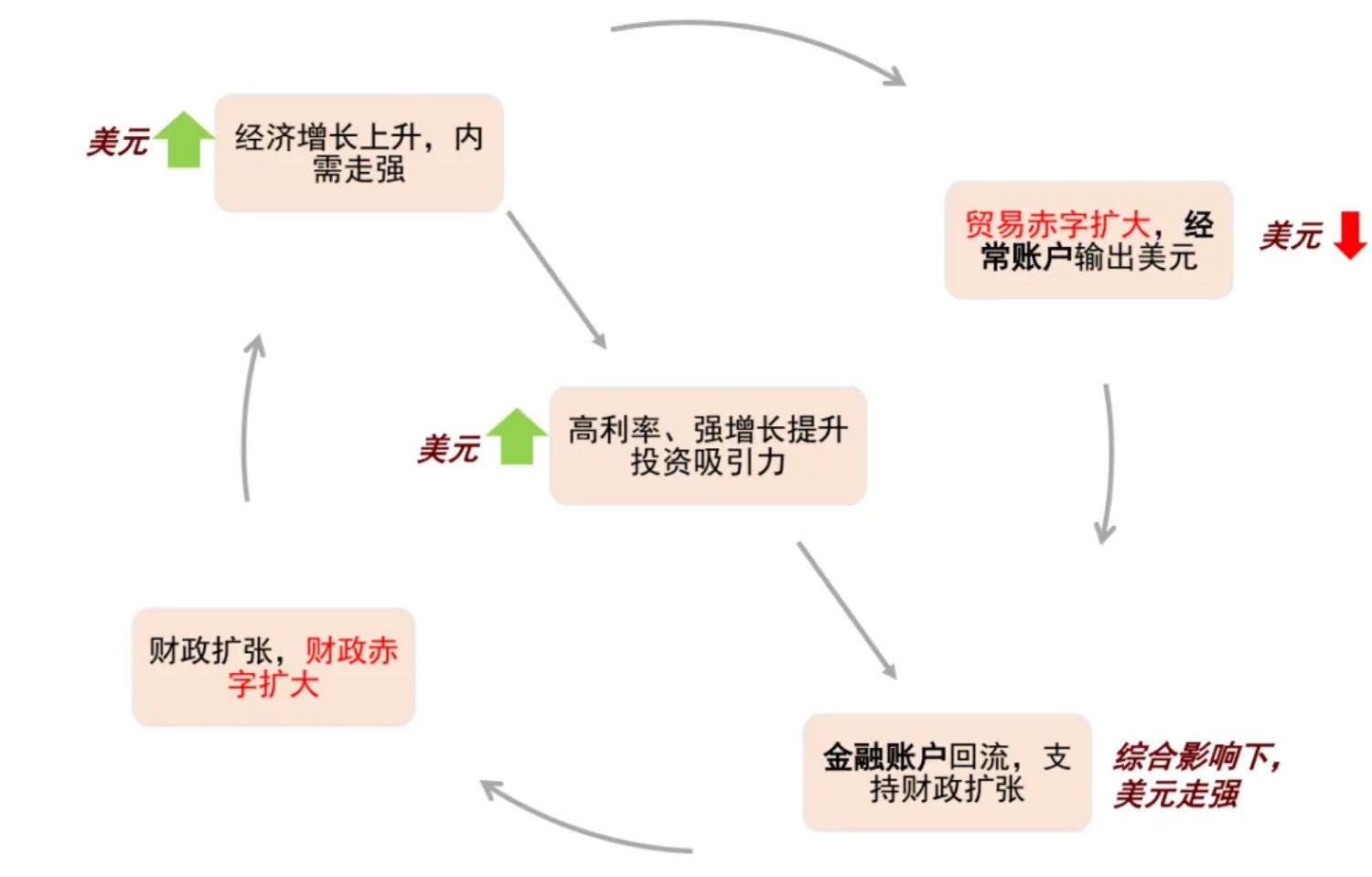

As a result, the United States formed a self-reinforcing “dollar cycle,” allowing the dollar to strengthen against the tide despite the U.S. twin fiscal and trade deficits. Price stability enhanced dollar credibility, high interest rates raised returns on dollar assets, growth recovery enhanced the appeal of U.S. assets, and capital inflows in turn provided financing support for U.S. fiscal expansion and financial-market prosperity. At the same time, the strong domestic demand brought by economic growth and a strong dollar expanded U.S. import demand, pushing up the trade deficit. And the dollar’s special status as an international reserve currency meant that the dollars flowing out through imports returned in the form of financial investment.

This mutually reinforcing process was summarized by Soros in The Alchemy of Finance as “Reagan’s Imperial Circle.” After 1983, the U.S. financial account turned to net inflows, which have continued to this day.

II. Why Open? Proactive Restructuring Under Passive Pressure—The Core Being That Capital Controls Harm Reserve-Currency Status in the Long Run

Taken together, the U.S. opening of its capital account in the 1970s, at a “fragile moment” of economic recession and dollar-credibility pressure, was essentially a proactive choice under passive shock.

It was “passive” because, after the collapse of the Bretton Woods system, the fixed-exchange-rate objective that capital controls were originally meant to serve had already become invalid; at the same time, the rapid expansion of the offshore dollar market made domestic capital controls increasingly difficult to enforce.

It was “proactive” because the United States realized that continuing to restrict capital outflows might not stop dollars from flowing out, but could instead weaken the central position of dollar assets and the New York financial market, ultimately damaging dollar credibility. Rather than clinging to an already-invalid closed framework, it was better to rebuild, through openness, the cycle of dollar funds “flowing out—flowing back.”

It is precisely in this sense that the U.S. capital-account opening in the 1970s was both a result of crisis-driven pressure and the starting point for a proactive restructuring of the dollar system.

Passive shock: The floating exchange-rate system weakened the necessity of capital controls, and the expansion of the offshore dollar system forced capital-account opening

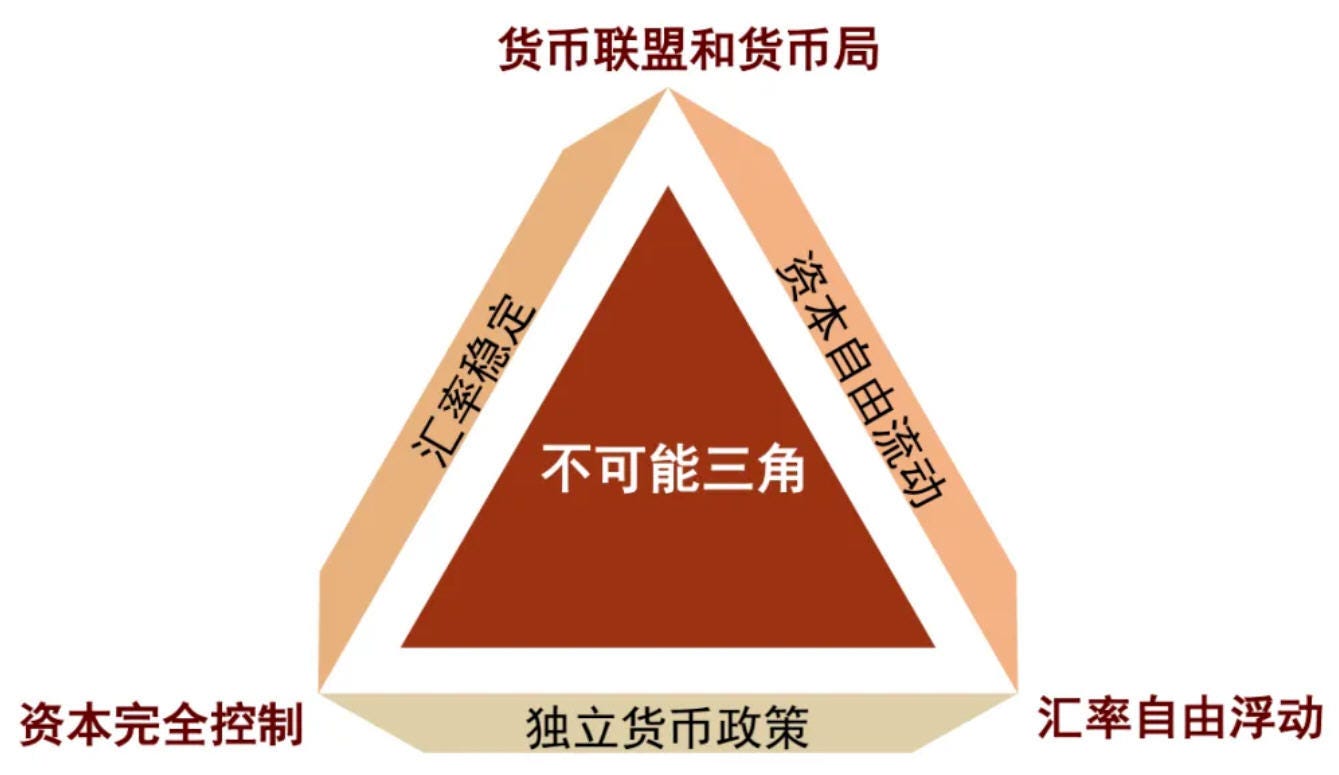

First, under the floating exchange-rate system after the collapse of Bretton Woods, the necessity of implementing capital controls declined. According to Mundell’s “impossible trinity,” a country cannot simultaneously achieve all three goals of fully independent monetary policy, exchange-rate stability, and free capital flows (Mundell, 1963; Obstfeld and Taylor, 1997). During the Bretton Woods period, countries in effect restricted capital flows as the price for obtaining fixed exchange rates and a degree of policy autonomy.

The U.S. restrictions on residents purchasing foreign securities, on bank overseas lending, and on corporate overseas investment were all aimed at reducing dollar outflows and gold-convertibility pressure. Volcker recalled that the U.S. capital controls of the 1960s came about when continuous capital outflows pressured the dollar, leaving the Treasury no choice but to use tools such as the Interest Equalization Tax (Volcker & Gyohten, 1992). However, the irreconcilable tension between fixed exchange rates and cross-border capital flows ultimately still dissolved the Bretton Woods system (Eichengreen, 1996; Obstfeld and Taylor, 1997); the fixed-exchange-rate system thereupon exited the stage, the institutional benefits of continuing capital controls declined, and the policy costs rose.

Second, the development of the offshore dollar market also forced the United States to loosen capital controls. The offshore dollar market (also known as the Eurodollar market) originated in the 1950s. After World War II, the United States continuously exported dollars to Europe through the Marshall Plan, overseas military spending, and overseas investment. Against the backdrop of the Cold War, countries such as the Soviet Union, in order to evade U.S. regulation, deposited dollars in the London banking system, and the earliest offshore dollar deposits were thus formed.

Entering the 1960s, financial regulatory measures within the United States further enhanced the appeal of the offshore dollar market. At the time, banks within the United States were constrained by “Regulation Q,” with caps on deposit interest rates, and also had to bear regulatory costs such as reserve requirements, whereas offshore dollar deposits were not subject to such constraints. For the same dollar liabilities, onshore costs were higher and constraints more numerous, while offshore costs were lower and restrictions fewer, giving funds and business an incentive to migrate to offshore markets (Friedman, 1971).

Against this backdrop, the offshore dollar market expanded. Friedman vividly likened the formation and expansion of the offshore dollar market to “the bookkeeper’s pen,” emphasizing that offshore dollars derived neither primarily from the U.S. balance-of-payments deficit or various central banks’ reserves, nor from the large-scale cross-border transfer of dollar cash, but were the result of credit creation by the banking system (Friedman, 1971). U.S. capital controls were facing a system that could continuously derive dollar credit beyond regulatory boundaries, rather than simple capital outflows.

However, Friedman did not believe the offshore dollar market could expand infinitely; he used “leakages” to explain the boundary of its credit derivation (Friedman, 1971). So-called leakage refers to dollars lent out by offshore banks that do not return to the Eurodollar banking system, but instead settle into deposits at U.S. domestic banks, are used for foreign exchange conversion or trade payments, or go into other asset allocation.

If a borrower, after obtaining dollars, deposits them in another offshore dollar bank, the new bank can continue lending after retaining a small amount of prudential reserves, and the offshore dollar multiplier rises; conversely, if the borrower uses the funds for payments, currency conversion, or deposits them in a non-Eurodollar bank (for example, depositing them back into a U.S. domestic bank), that portion of funds is equivalent to “leaking out” of the Eurodollar system, the credit chain is broken, and the derivation multiple declines accordingly.

The lower the leakage, the higher the offshore re-deposit ratio, and the more easily dollar credit can be derived layer by layer overseas; the higher the leakage, the closer offshore activity comes to a one-off bookkeeping transfer, and the weaker the multiplier effect. Therefore, regulatory arbitrage opened up the space for offshore dollar credit creation, while leakage determined the extent to which derived credit could be magnified.

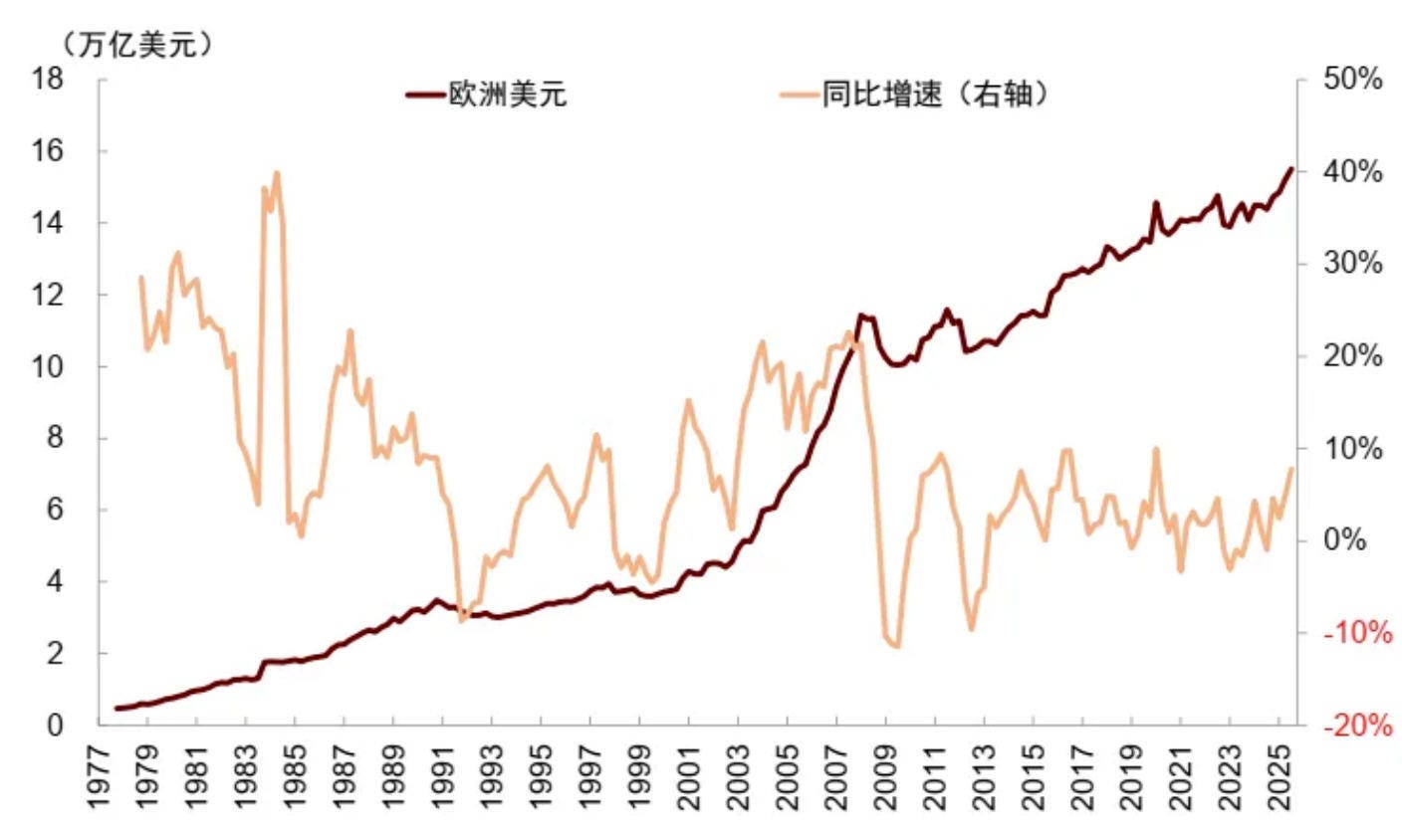

Even with the constraint of leakage, the offshore dollar market had already reached a considerable scale by the early 1970s. According to BIS statistics, by the end of 1973 the external dollar liabilities of reporting European banks had reached 130 billion dollars and external dollar assets nearly 134 billion dollars, having grown roughly tenfold in just seven years, with an average annual expansion rate of 20–30%—far exceeding the growth rate of the U.S. domestic money supply over the same period.

Even after deducting the double-counting caused by re-deposits within the European banking system, the dollar credit scale estimated by the BIS for 1973 was still about 97 billion dollars. This scale was equivalent to 7% of U.S. GDP in 1973, 1.4 times the full-year merchandise imports, and 53% of total global official reserves—already enough to affect dollar funding costs, cross-border credit allocation, and the competitiveness of the New York financial center.

Thus, the growth of the offshore dollar market created pressure compelling the United States to open its capital account. On the one hand, the rapid expansion of the offshore dollar market rendered capital controls “existent in name only.” Global demand for dollars did not weaken because the United States tightened onshore controls; instead, it shifted more toward the offshore dollar market.

In a 1971 memorandum, Shultz pointed out that the effectiveness of capital control measures was questionable: the Interest Equalization Tax reduced foreign securities purchases, but this gap was quickly diluted by increases through channels such as U.S. direct investment and bank loans; and although foreign credit restraints once curbed short-term private U.S. capital outflows, this positive effect was almost entirely offset by reverse changes in foreign private short-term capital flows. Therefore, capital controls did not truly improve the balance of payments, and even brought economic-efficiency losses and administrative costs.

On the other hand, this also put pressure on the pricing system of the onshore dollar financial system. The offshore market could conduct dollar business at lower cost, gradually forming an offshore interest-rate system represented by LIBOR. Volcker also pointed out that if the United States continued to insist on capital controls, demand for dollar funding and trading would still exist; global dollar business would not disappear, but would simply shift more to offshore centers such as London, the Bahamas, and Luxembourg, harming New York’s intermediary and pricing position in global dollar funding (Volcker & Gyohten, 1992).

Proactive choice: Strengthening the dollar’s reserve-currency status; the neoliberal current of thought provided the policy atmosphere; an opportunity to re-steady the dollar system

Beyond the passive adjustment driven by external shocks, the U.S. choice to open its capital account in 1974 also had its proactive strategic considerations. First, the foundation of openness lay in the dollar’s reserve-currency status. After the collapse of the Bretton Woods system, the dollar’s share of reserve currencies declined somewhat, and although there was still no currency that could replace the dollar (There is no alternative, TINA), concerns persisted that long-term capital controls would weaken the usability and credibility of dollar assets.

Volcker recalled that Shultz and others had real reasons for opposing capital controls: the effectiveness of controls was increasingly limited, the distortions increasingly large, enforcement increasingly difficult, and they had become a burden on businesses and financial institutions (Volcker & Gyohten, 1992).

In addition, the “neoliberal” current of thought in the 1970s also provided the policy atmosphere for the United States to open its capital account. The stagflation shock of the 1970s weakened the Keynesian policy consensus, “neoliberalism”—with monetarism and free markets as its main ideas—rose, and financial liberalization gradually became the mainstream policy direction (Harvey, 2005).

Volcker recalled that officials such as Shultz were deeply influenced by Friedman and believed that markets could allocate capital better than governments (Volcker & Harper, 2018). Simon, too, repeatedly emphasized in his memoirs his opposition to government control and his advocacy of a return to free-enterprise principles (Simon & Caher, 2003).

Against this backdrop, the United States realized that opening the capital account was not merely a source of risk, but could also become an opportunity to re-steady the dollar system. As the issuer of the reserve currency, although lifting capital restrictions might cause dollar outflows, paths such as global trade, reserves, and safe-asset allocation were still creating demand for dollars. Therefore, rather than clinging to invalid capital controls and watching the offshore market erode the influence of the New York financial center, it was better to open proactively, leveraging the depth and liquidity of U.S. financial markets to re-absorb global funds—including petrodollars—back into the domestic system, consolidate the position of the New York financial center, and rebuild the dollar cycle to steady the dollar’s hegemonic position. Dollars would flow out, but they would also flow back through global dollar demand, the allocation of oil-producer surplus funds, and the depth of U.S. financial markets.

Smooth operation after opening: The depth of financial markets and technological/institutional advantages were important supports

After the United States opened its capital account in 1974, no stable net foreign inflows formed in the initial period, and it even bore net capital-outflow pressure for a time. But these outflows did not evolve into uncontrolled capital flight, and the dollar system did not collapse as a result. The reason was that behind it lay financial markets deep enough to absorb the funds, relatively mature payment-clearing and trading infrastructure to support liquidity, and relatively complete institutional arrangements to stabilize expectations. This was specifically reflected in the following three aspects:

► Market depth: The Treasury market was large in scale and strong in liquidity, serving as an important safe-asset pool for global capital. By the 1970s the United States had gradually formed relatively mature mechanisms for Treasury issuance, pricing, and trading; medium- and long-term Treasuries began to be auctioned regularly, and short-term Treasury Bills were continuously rolled over.

At the same time, multi-tiered short-term money markets—including the federal funds market, large negotiable certificates of deposit (CDs), and the repo market—also developed rapidly, reducing friction costs for the banking system’s liquidity allocation (Gorton, 2010).

► Technological advantages: In the 1970s the technology supporting cross-border capital flows became increasingly mature; the Clearing House Interbank Payments System (CHIPS) and the Society for Worldwide Interbank Financial Telecommunication (SWIFT) were established in 1970 and 1973, respectively. Among them, CHIPS served large-value net dollar payments and was widely used for settlement related to foreign exchange and securities trading, serving as the core clearing infrastructure supporting cross-border dollar transactions; SWIFT promoted the standardization of cross-border financial communication, facilitating cross-border capital flows.

► Institutional completeness: Financial regulatory systems were mature; domestically, the securities market had established a regulatory system under the U.S. Securities and Exchange Commission (SEC), the banking system had deposit insurance provided by the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve assumed the lender-of-last-resort function. Externally, the Treasury maintained dollar stability through the U.S. Treasury’s Exchange Stabilization Fund (ESF), while the Federal Reserve established liquidity-support mechanisms with major central banks through central-bank swap lines—together constituting the institutional support for the dollar’s external stability.

Volcker mentioned in his memoirs that Robert Roosa called these official financial innovations the “inner and outer lines of defense” for protecting the dollar and the international monetary system (Volcker & Gyohten, 1992); the existence of these arrangements shows that even as the United States loosened capital controls, it did not abandon management of the dollar system.

From this it can be seen that capital-account opening did not occur after “everything was ready”; it was more a trade-off made when old constraints were gradually loosening and a new cycle had not yet formed. Other countries had similar experiences. In October 1979 the United Kingdom lifted its remaining foreign-exchange controls, facing the decline of sterling’s status and pressure to reposition the London financial center; had it continued controls, it might not have held onto sterling, but could have lost its financial center. In 1979 Japan revised its Foreign Exchange and Foreign Trade Control Law, shifting from “prohibition in principle” to “freedom in principle”; West Germany in 1981 basically removed remaining restrictions on capital inflows and in 1984 further abolished the withholding tax on non-residents holding German bonds—facing current-account surpluses, currency appreciation, and demand for capital export; had they continued to remain closed, the external surpluses accumulated by the real sector would have been hard to convert into international financial influence.

Therefore, the key to capital-account opening lies not in waiting for a moment of complete stability and the right internal and external environment, but in whether, under controllable risk, passive shocks can be transformed into proactive restructuring, and whether dynamic adjustments can be continuously made during the opening process—to magnify the benefits of opening and shrink the risks of opening.

III. Lessons for Renminbi Internationalization? Establishing a Mindset of “Dynamic Trade-offs” in Opening; Capital-Account Opening and Currency Internationalization Dynamically Reinforce Each Other

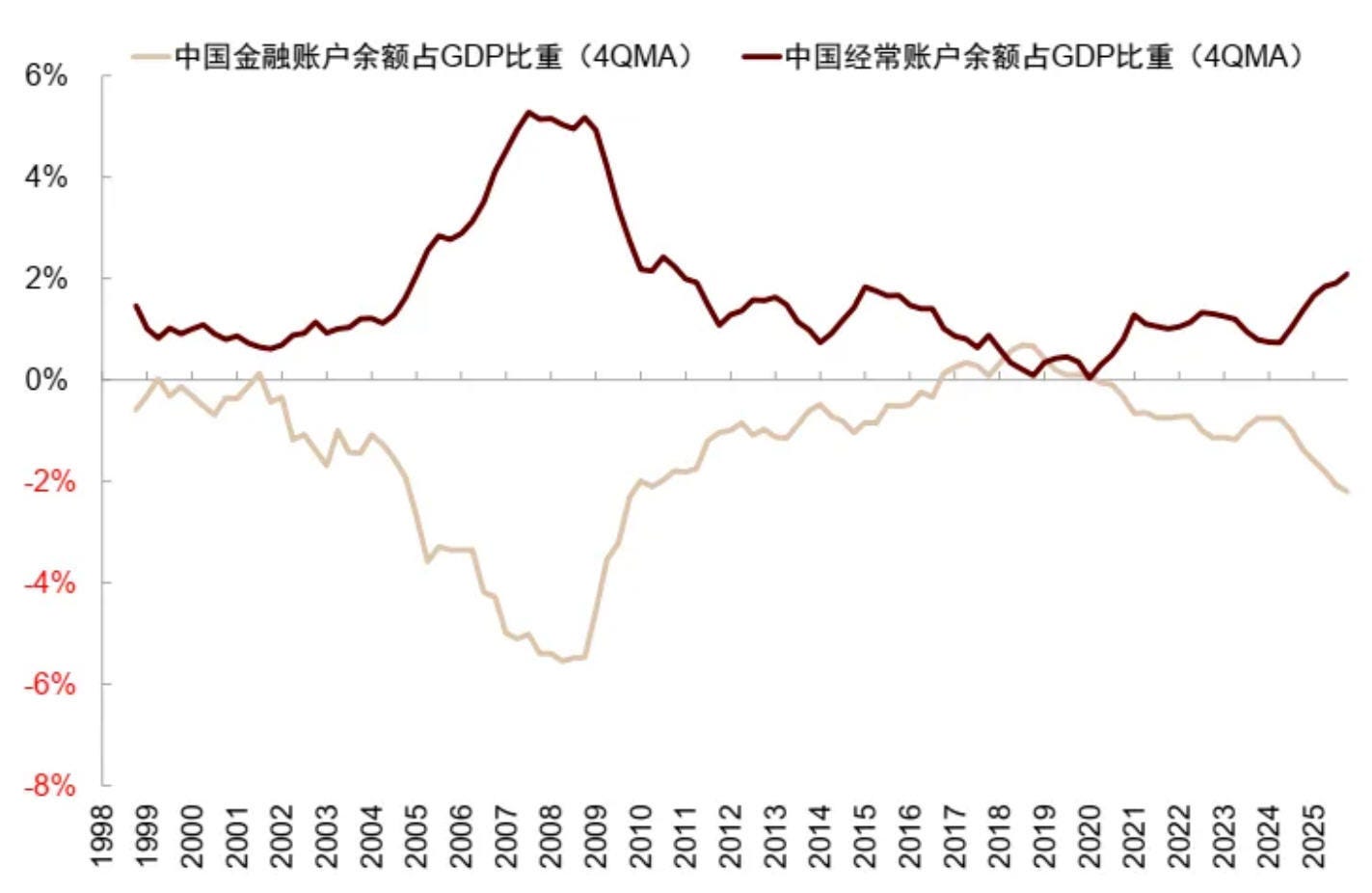

At present, China stands at a critical historical juncture for steadily expanding institutional opening and promoting renminbi internationalization during the “15th Five-Year Plan.” According to the IMF’s classification of capital-account transactions, China has achieved varying degrees of convertibility for most items, but a few sub-items still implement relatively prudent management; compared with major reserve-currency economies, there is still room to raise the actual degree of financial openness. Concerning capital-account opening, the most common market concern is: will further raising the level of capital-account openness lead to large-scale capital outflows?

Referring to the U.S. experience, the early stage of capital-account opening may indeed bring the pain of capital outflows. But the crux of the matter lies not in whether capital outflows occur in the early stage of opening, but in whether a sustainable funding cycle can form after opening—and this ultimately depends on whether prices are stable and growth is robust.

In the early stage of currency internationalization, capital-account opening is not a precondition; but in the long run, an internationalized currency must be freely convertible. As a reserve currency, it must open its capital account, exporting liquidity overseas, while overseas demand in turn prompts the currency to flow back, forming a cycle of two-way flows.

The history of U.S. capital-account opening is, in essence, a history of dynamic trade-offs between strengthening reserve-currency status and maintaining financial stability. In this process of dynamic balance, the reserve-currency dividend and the financial-stability risk brought by opening are not fixed. In the long run, once the internationalization network and the reflux mechanism mature, the institutional benefits brought by opening will continue to magnify, and the financial system’s resilience to risk will also continuously strengthen amid the two-way cycle.

The U.S. case shows that the reason capital-account opening was ultimately able to strengthen the dollar system lies not in opening itself, but in the institutional synergy formed among opening, floating exchange rates, offshore-market development, financial-market depth, and macroeconomic stability.

First, long-term capital controls weaken the availability and credibility of reserve-currency assets, ultimately disadvantaging reserve-currency status. Second, floating exchange rates and offshore-market development are important conditions for the capital account to be able to withstand the shocks of two-way flows. Third, whether funds can continuously flow back after opening depends on whether the home country’s assets are sufficiently attractive—which in turn depends on price stability, growth resilience, and financial-market depth.

Thus, the lessons for renminbi internationalization are as follows:

► Establish a mindset of “dynamic trade-offs” in opening, driving a “Pareto improvement” in macro-finance through high-level opening to the outside world. For the United States in 1974, between the risk of capital outflows and the benefit of consolidating reserve-currency status, it chose to open its capital account. Although it faced the pain of capital outflows and exchange-rate depreciation in the early stage, it ultimately still became the starting point for strengthening the dollar’s status.

For China, “no sugarcane is sweet at both ends”—there is no completely risk-free shortcut to capital-account opening, and the process of opening must be a dynamic trade-off between risk and benefit. Statically, relaxing capital controls a bit more seems to mean exposing a bit more outflow risk. However, dynamically, long-term closure also comes at a cost. If renminbi assets are difficult for overseas entities to conveniently hold and allocate, the renminbi will struggle to move further from a settlement currency to an investment currency and a reserve currency, and thus will be unable to obtain the reserve-currency dividend.

Therefore, the significance of high-level institutional opening is not simply to enlarge risk exposure, but to reshape the risk-return combination at a higher level, achieving a “Pareto improvement” in the macro-financial sense: enhancing both the efficiency of resource allocation and the appeal of renminbi assets, while also—through more mature market pricing, richer risk-hedging tools, and a more complete macroprudential framework—improving the entire economy’s ability to withstand external shocks. In other words, opening is not about sacrificing safety for efficiency, but about simultaneously enhancing both efficiency and safety at a higher level.

Just as a person can only learn to swim in the water, the renminbi must also learn to open within openness; it cannot learn to open within closure. Actively advancing high-level institutional opening, in an environment of two-way capital flows, helps market participants better develop pricing, hedging, and risk-management capabilities, and only thus can the macro-policy framework be continuously improved. From this, the renminbi can achieve a dynamic unity of high-level development and high-level security, and the process of dynamic capital-account opening will also mutually reinforce the historical process of renminbi internationalization.

► Increase exchange-rate flexibility, and coordinate the development of onshore and offshore renminbi markets. An important precondition for the U.S. opening of its capital account in 1974 was the floating exchange-rate system after the collapse of the Bretton Woods system; exchange-rate floating is the “safety valve” of capital-account opening, capable of relieving the pressure of large capital inflows and outflows.

In addition, the pressure from offshore markets was an important reason the United States loosened capital controls, while the depth of the onshore market provided a key condition for the United States to open its capital account. Only through the coordinated development of onshore and offshore markets can a solid and sustainable institutional foundation be provided for renminbi internationalization. In the onshore market, market depth can be enhanced by improving the liquidity of the secondary market for Chinese government bonds and enriching interest-rate risk-hedging tools; in the offshore market, efforts should focus on developing the Hong Kong offshore renminbi financial market, promoting offshore renminbi bond issuance, enriching financial products in the offshore renminbi market, and improving offshore renminbi market infrastructure.

► Seize opportunities to actively promote renminbi-denominated settlement and improve the “renminbi cycle” mechanism. The reason funds did not evolve into long-term large-scale capital flight after the United States opened its capital account lies chiefly in the “petrodollar” mechanism and in the asset appeal brought by U.S. price stability and strong economic growth in the 1980s, which together drove the formation of the “dollar cycle.”

For China, to form a “renminbi cycle,” it should first broaden the channels for exporting renminbi liquidity overseas. Obstfeld (2026) pointed out that the export of dollar liquidity does not necessarily occur through a current-account deficit; it can also occur through outward investment via the capital and financial accounts, or through credit creation in the offshore dollar market. In the 1960s, the United States was still running a current-account surplus, but the offshore dollar market was already able to derive dollar liquidity overseas through the banking system. Similarly, while maintaining a current-account surplus, China can also export renminbi liquidity through the “Belt and Road,” enterprises going overseas, outward investment, and other means.

In addition, it can also seize the opportunities brought by external shocks and global industrial transformation, actively promoting renminbi-denominated settlement and the reflux of renminbi funds. China is the world’s largest manufacturing center, an important importer of energy and commodities, and has strong industrial influence in fields such as new energy, strategic minerals, and green industries. In the future, it can explore raising renminbi settlement and pricing in key resource goods such as strategic minerals, the “new three” [New energy vehicles, lithium batteries, and photovoltaic products], and even computing power.

Finally, stable prices, deep financial markets, and stable growth are key to attracting funds to continuously flow back. Overseas entities being willing to accept renminbi is only the first step of renminbi internationalization; being willing to invest in and hold renminbi assets over the long term is the key to the renminbi moving from a settlement currency to an investment currency and a reserve currency.

The reason the United States attracted funds to flow back after opening in the 1980s still lay chiefly in the asset appeal brought together by the price stability following Volcker’s inflation control and the growth vitality unleashed by Reagan’s supply-side economics. In the long run, only by building an internal ecosystem with stable prices, more resilient growth, sufficient market depth, and attractive asset returns can funds be attracted to flow in sustainably over the long term amid the dynamic allocation of global capital.

Yes, if China wants RMB to become a global reserve currency, it has to open up the capital account. However, I see zero evidence that the Chinese government wants this to happen. I think the ultimate question is whether it will benefit the Chinese people. After witnessing the costs that American people payed, such as deindustrialization, over financialization, large military spending, etc. I doubt Chinese people want the Yuan to be the next reserve currency. A better approach is a new multipolar currency basket.