Is China's Trade-In Policy Working?

Economist Li Xunlei calls for shifting from subsidizing durables to boosting services, jobs, and incomes for the many

It has been two years since the Chinese government initiated its trade-in policies to boost domestic demand, and the results are due for a hard look. Li Xunlei, chief economist at Zhongtai Securities and a veteran of three decades in macroeconomic and capital-market research, provides exactly that in his article.

He’s also an influential figure in policy circles; last year, he joined Premier Li Qiang's April 9 symposium on economic conditions alongside other leading experts and business leaders.

His research found that while the program successfully stimulated consumption in the short term, diminishing marginal returns are also evident. Consumers who have already traded in their durable goods are unlikely to do so again anytime soon. Moreover, automobiles alone accounted for over 60% of the total sales driven by the subsidies, suggesting that the primary beneficiaries have been middle- to high-income groups, whose marginal propensity to consume is low. A significant portion of the fiscal spending did not generate incremental consumption, but rather amounted to a windfall for people who would have made these purchases anyway.

He calls for expanding the program's overall funding while fundamentally redesigning its direction — extending coverage to service consumption, lowering the average price threshold of subsidized goods to reach more low- and middle-income consumers, and shifting the policy objective from simply 'boosting sales figures' toward the more fundamental goal of 'promoting employment and raising incomes.

Below is his full text published on his WeChat account:

How to Expand Beneficiary Coverage of the “Trade-In” Program

During 2024–2025, the central government allocated a combined RMB 450 billion in ultra-long special government bond funds to support the consumer goods “trade-in” policy, delivering subsidies directly to consumers totaling over 480 million person-times—of which over 120 million person-times occurred in 2024, over 280 million in the first half of 2025, and over 80 million in the second half of 2025. The program drove related merchandise sales exceeding RMB 2.6 trillion and directly contributed 0.6 percentage points to the growth of total retail sales of consumer goods.

These figures reveal two salient features of the policy. On one hand, the trade-in program has been indispensable in boosting consumption—without it, achieving the 5% growth target in 2025 would have been difficult. On the other hand, the policy’s multiplier effect appears to have fallen short of expectations, and its beneficiary pool remains relatively narrow. Since May 2025, the year-over-year monthly growth rate of total retail sales of consumer goods has decelerated steadily, reaching only 0.9% in December. Moreover, the number of beneficiary person-times in the second half of 2025 declined to just 80 million. This paper explores how to enhance the marginal effectiveness of the trade-in program, expand its beneficiary coverage, and promote employment.

The “Trade-In” Policy: From Launch to Enhancement to Expansion

In July 2024, the State Council issued the Notice on Several Measures to Strengthen Support for Large-Scale Equipment Renewal and Consumer Goods Trade-In, earmarking approximately RMB 150 billion in ultra-long special government bond funds for local governments to support consumer goods trade-ins. In 2025, an additional RMB 300 billion was allocated to support the scaling-up and broadening of the trade-in program, expanding eligible home appliance categories from 8 to 12 and introducing purchase subsidies for smartphones and other digital products.

[Chart 1: Estimated Sales Driven by the Trade-In Program]

How Effective Has the Trade-In Program Been in Driving Consumption?

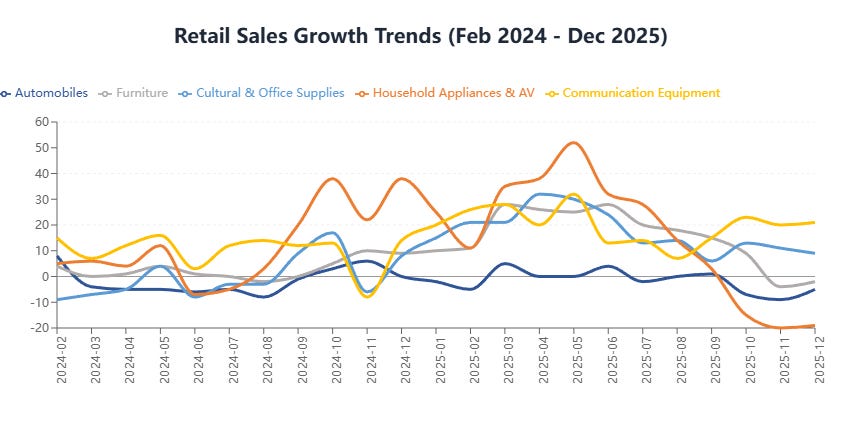

Looking at retail sales across the five major product categories associated with the trade-in program, year-over-year growth rates generally followed a pattern of initial acceleration followed by deceleration. In 2025, among above-designated-size retail units, retail sales of telecommunications equipment and cultural & office supplies grew by 20.9% and 17.3% year-over-year respectively, maintaining double-digit growth across all four quarters. In contrast, while full-year retail sales of household appliances & audio-visual equipment and furniture grew 11% and 14.6% respectively, monthly growth rates had already turned negative. Growth in automobile consumption lagged behind overall merchandise consumption.

[Chart 2: Monthly YoY Growth of Trade-In Related Retail Sales (%)]

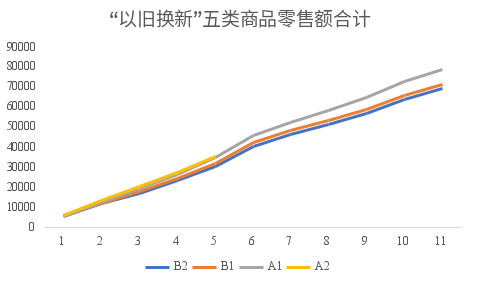

Given that funding support began in August 2024 (the national-level policy was issued on July 24, 2024; we temporarily set aside the time lag between local implementation guidelines and actual policy rollout), and to eliminate base effects and seasonal distortions, we divide the observation period into four segments:

Before2 (B2): Aug 2022 – Jul 2023, the second complete year before policy implementation

Before1 (B1): Aug 2023 – Jul 2024, the first complete year before policy implementation

After1 (A1): Aug 2024 – Jul 2025, the first complete year after policy implementation

After2 (A2): Aug 2025 – end of 2025, the second (incomplete) year after policy implementation

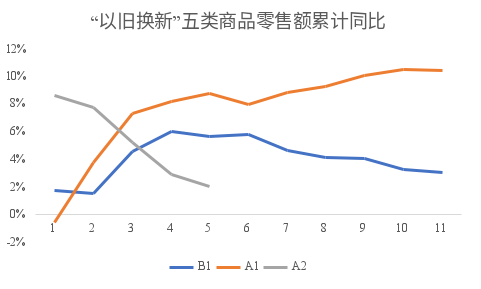

The data shows that in the first complete year after implementation (A1), retail sales of related product categories grew by 10%, significantly outpacing the pre-policy period (approximately 3% annual growth, B1). However, in the second incomplete year (A2), growth was only about 2% over the same period of the first post-policy year—well below the roughly 9% growth recorded when comparing the first post-policy year to the pre-policy baseline.

[Chart 3: Cumulative Retail Sales of Trade-In Related Products (RMB 100 million)]

Examining cumulative year-over-year growth rates, the first full year after implementation showed a marked acceleration compared to the pre-policy period, while the second year saw a notable decline.

[Chart 4: Cumulative YoY Growth of Trade-In Related Retail Sales (%)]

Are subsidies merely producing a pulse effect on retail sales? We applied the above methodology to each of the five major product categories and found the following:

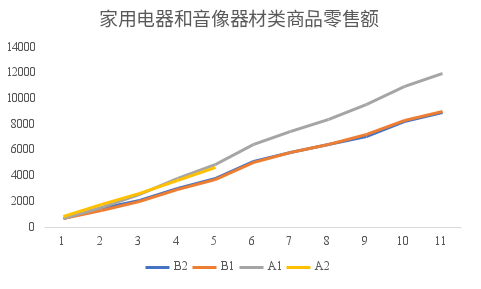

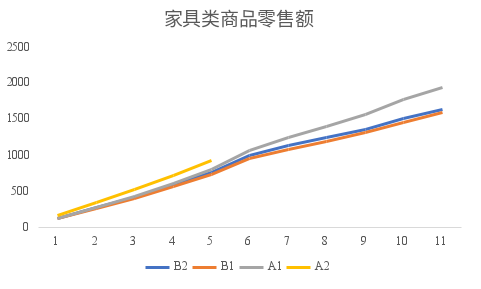

(1) The “enhancement” effect is evident in the first year, but sustaining rapid retail sales growth may prove difficult. The allocation of ultra-long special government bond funds starting in August 2024 had a significant positive impact on related retail sales—B1 and B2 largely overlap in the charts, while A1 shows a clear upward shift from B1. However, in the second year, the stimulative effect weakened markedly (A2). A likely explanation is that consumers who have already upgraded durable goods such as home appliances are unlikely to do so again in the near term.

[Chart 5: Cumulative Retail Sales of Household Appliances & Audio-Visual Equipment (RMB 100 million)]

[Chart 6: Cumulative Retail Sales of Furniture (RMB 100 million)]

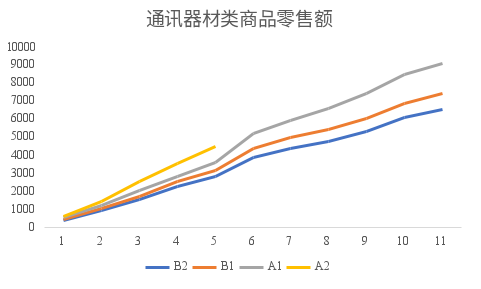

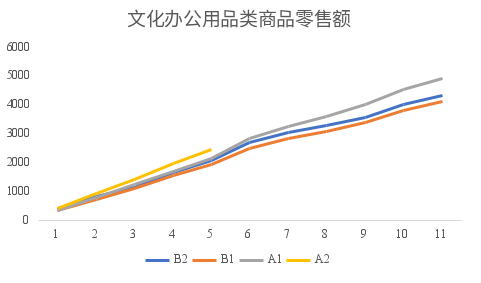

(2) “Broadening” the scope can sustain retail sales growth even against a high base, since newly covered products are effectively in their “first year” of subsidies. In 2025, purchase subsidies were introduced for the first time for individual consumers buying smartphones, tablets, and smartwatches/bands. Accordingly, retail sales of telecommunications equipment and cultural & office supplies continued to grow meaningfully on top of already elevated growth rates—even though A1 already stood well above B1, A2 still showed notable growth over the same period in A1.

[Chart 7: Cumulative Retail Sales of Telecommunications Equipment (RMB 100 million)]

[Chart 8: Cumulative Retail Sales of Cultural & Office Supplies (RMB 100 million)]

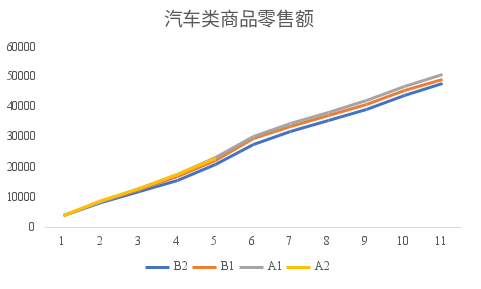

(3) The automobile trade-in subsidy has had limited impact on retail sales. Although in 2025 one out of every two new passenger cars sold benefited from a trade-in subsidy, the stimulative effect on automobile retail sales was noticeably weaker than for the other four product categories. Possible explanations include: the high unit price of automobiles makes purchases more sensitive to macroeconomic factors such as income and expectations; consumers who already intended to buy or replace a vehicle likely simply applied for the subsidy rather than being induced to purchase by it; and the industry’s “trading price for volume” dynamic, in which widespread price cuts offset the growth in unit sales.

[Chart 9: Cumulative Retail Sales of Automobiles (RMB 100 million)]

Of course, the trade-in program should not be assessed solely through the lens of consumer subsidies. The policy also promotes green production and consumption patterns, accelerates the development of recycling systems, and improves product safety.

(1) Energy conservation and carbon reduction. Green, low-carbon products have been adopted at an accelerating pace: nearly 60% of vehicles purchased by consumers were new energy vehicles, and over 90% of home appliances purchased were rated at the highest tier of energy or water efficiency. The “Two Renewals” policies (including trade-ins) have cumulatively generated annual energy savings exceeding 69 million tonnes of standard coal equivalent and reduced carbon emissions by over 170 million tonnes.

(2) Recycling. The recycling and reuse infrastructure has been significantly strengthened. During 2024–2025, over 29,000 smart community recycling facilities were added nationwide; 17.673 million end-of-life vehicles were recycled, with an average annual growth rate of 45.8%; 39.686 million used vehicles were traded; and approximately 53 million units of waste home appliances and mobile phones were formally dismantled, with an average annual growth rate of roughly 12%.

(3) Safety improvements. In 2025, the number of outdated electric bicycles retired and replaced was more than nine times the 2024 figure. All replacement electric bicycles carry product certificates and CCC certifications compliant with current national standards, and approximately 90% use lead-acid batteries, which offer superior safety performance.

The 2026 Consumer Goods Trade-In Policy: Can Beneficiary Coverage Be Expanded?

On December 30, 2025, the Ministry of Commerce and six other government departments issued the Notice on Enhancing Quality and Efficiency in Implementing the 2026 Consumer Goods Trade-In Policy. Compared with 2025, the policy includes the following adjustments: (1) Adjusted subsidy scope. Smart glasses have been added as a new category under digital and smart products. (2) Unified subsidy standards. In line with the goal of building a unified national market, uniform subsidy standards are now applied nationwide for automobile scrappage renewal, automobile replacement renewal, six categories of home appliance trade-ins, and four categories of digital and smart product purchases. (3) Optimized subsidy mechanisms. The fixed-amount subsidy for automobile scrappage/replacement renewal has been converted to a proportional subsidy, with the maximum cap unchanged. (4) Strengthened energy-efficiency orientation. Home appliance subsidies are now restricted to Tier-1 energy/water-efficiency products, and the subsidy rate has been reduced from 20% to 15%.

These adjustments are intended to address several considerations. First, amplifying policy impact—leveraging fewer fiscal resources to drive greater consumption growth. Second, enhancing fairness and inclusiveness—for instance, switching from fixed-amount to proportional subsidies for automobiles (which carry larger per-unit subsidies) implements a “spend more, get more” approach within the cap. Third, “embracing innovation”—including smart glasses in the subsidy scope aligns with the trend of AI wearable devices going mainstream, lowers the barrier to experiencing cutting-edge technology, and fosters a virtuous cycle where new demand guides new supply and new supply creates new demand.

These policy rationales are all well-founded. However, a notable concern is that the number of beneficiaries over the past two years has been relatively modest—only a cumulative 480 million person-times. Measured by unique individuals, the figure is likely even smaller, with trade-in participants potentially accounting for less than one-third of the total population. This is particularly evident in the second half of 2025, when beneficiary person-times dropped sharply to 80 million, signaling a declining marginal impact.

China’s primary consumer demographic should be the low- and middle-income population, comprising approximately 60% of the total population, or 840 million people. However, the main beneficiaries of the trade-in program have been high-income and upper-middle-income groups (per the National Bureau of Statistics’ classification), primarily because the average unit price of subsidized products skews high—automobiles, for example, accounted for 61.5% of total trade-in-driven consumption in 2025. Given the high unit price of automobiles, beneficiaries are predominantly high-income individuals whose marginal propensity to consume is low; they would likely have purchased new vehicles even without subsidies. Meanwhile, the ongoing price war in China’s automobile industry has already eroded profit margins significantly and intensified overcapacity pressures—further encouraging industry expansion would be ill-advised.

To expand beneficiary coverage of the trade-in program, the following measures merit consideration:

(1) Increase funding and broaden product categories. Could the 2026 allocation be expanded from the 2025 level of RMB 300 billion to RMB 400 billion? Could eligible categories be extended beyond durable consumer goods to encompass daily necessities, general merchandise, and even services under a “national subsidy” framework?

(2) Lower the average unit price of subsidized products to better stimulate purchasing willingness among low- and middle-income groups. For example, the multiplier effect of electric bicycle trade-ins significantly exceeds that of automobiles.

(3) Shift the program’s objective from “treating the symptoms” to more fundamentally “addressing root causes”—namely, promoting employment, raising incomes, and stabilizing expectations. Policymakers may be primarily evaluating the program based on the volume of consumption it generates, but such sales increases may be one-off in nature. Even a massive automobile trade-in program contributes little to employment, as manufacturing employment has been declining since 2013. Given that China’s service sector still accounts for a relatively low share of total employment, increasing trade-in support for service consumption could play a meaningful role in boosting service-sector employment.