A Counterargument to The Economist's "China's World-Beating Solar Industry Is in Turmoil"

David Fishman on why the "turmoil" framing misreads China's solar sector, and what's actually happening as the industry leaves policy protection behind

Recently, The Economist published a piece China’s world-beating solar industry is in turmoil, saying that despite producing over 80% of the world’s solar panels, China’s solar industry is in serious trouble—and that even the temporary export boost from the US-Iran war hasn’t steadied it. The Economist said three converging problems have left most companies running at a loss since 2024: falling domestic demand, oversupply, and rising protectionism in Western markets.

But David Fishman, a long-term researcher of the Chinese new energy sector pointed out some of the framing and epistemic problems of the article. He argued that the “turmoil” is better understood as a structured transition. When policy protection was pulled out, and the industry was exposed to the real market, such friction is predictable. Or, to put it in our Chinese words, it’s 发展中出现的问题, and it has to be 靠发展解决—problems that emerge in the course of development, which can only be solved by further development.

In his view, the piece oversimplifies why domestic demand is softening, treating it as a story about grids becoming overloaded with solar when the real driver is the shift away from generous feed-in tariffs toward market-based pricing.

He also believes the article gets the cause and effect on curtailment backwards, describing it as a problem of too much solar when it is really a problem of insufficient grid flexibility. He thinks that the piece mischaracterizes the coal-versus-renewables dynamic, which has less to do with one fuel locking out another and more to do with the basic tension between forward contracting and real-time markets.

Finally, he questions how the article reads both the export picture and the wave of company bankruptcies, suggesting that if oversupply is truly the core problem, then firms exiting the market should count as part of the solution rather than a sign of gloom.

In the end, he argues, the article never lands on a coherent thesis tying its negative data points together.

I decided to share his correction of the article as a sort of contribution to understanding the Chinese new energy sector.

David Fishman currently works for the Lantau Group, where he specializes in China’s power sector. His work covers solar, wind, coal, nuclear, hydro, transmission, and power markets, with particular focus on renewable energy policies and market forecasting. Before joining Lantau Group, Fishman was Managing Co-Director of Shanghai-based Nicobar Group, a nuclear energy consultancy. He holds a joint MA in International Relations and Energy Policy from Johns Hopkins SAIS and Nanjing University, and is fluent in Mandarin Chinese.

He’s also the founder of a newsletter Crossing the River by Feeling the Stones where he provides first-hand observations on Chinese rural areas and poverty alleviation efforts. His conversations with locals offer valuable grassroots perspectives on China’s development, which I really enjoyed.

Thanks to Mr. Fishman for allowing me to repost his counterargument in my newsletter. Below is his piece, as published on LinkedIn.

This is a Structured Transition, Not Turmoil: Responding to The Economist’s Coverage of China’s Solar Sector

Last week The Economist ran this piece (link paywalled) titled “China’s world-beating solar industry is in turmoil“:

While it does cover some important and correct aspects of the current challenges in China’s solar sector, including low panel prices and a slowdown in capacity growth, I also found a number of problems with the piece - both epistemic and in framing/presentation.

I then became increasingly concerned to see the piece start to be quoted in some of my industry circles. This prompted me to prepare a response for Twitter/X, which I will now reproduce here on LinkedIn as well.

For each section, I will provide a screenshot of text from The Economist article, with relevant sections highlighted in yellow and my commentary following the screenshot. Let’s start:

1) Oversimplification

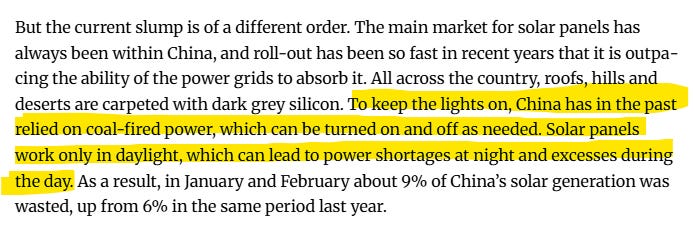

Unfortunately, it is a major oversimplification to say Chinese domestic demand for solar panels is falling “because the country’s power grids have become overloaded with the things”.

The real challenge right now is developers and banks still figuring out how to finance and build projects without policy-backed revenue guarantees. Domestic demand was shored up in past years by a generous feed-in-tariff (FiT) scheme that ensured stable and predictable revenues. Following the the longstanding policy trend toward liberalization, last year solar generators were shifted out of FiTs and into a Contract-for-Difference (CfD) scheme. Guaranteed CfD volumes have quotas, with non-CfD volumes expected to find customers via open markets (i.e. merchant exposure). The piece acknowledges the policy change from last year, but doesn’t seem to recognize the importance.

New solar capacity growth will likely be flat or even decline YoY in 2026 because generators and financiers are still inexperienced with merchant risk and renewable consumption quotas aren’t quite high enough yet to drive more long-term renewable power contracting demand (which financiers rely on).

Yes, low prices in daytime spot power markets reflect temporal oversupply, but that’s largely irrelevant for investment decisions, which are built around long-term contracts, not spot markets.

2) Misdiagnosis

The cause-and-effect relationships in this paragraph are backwards.

If you’re explicitly trying to build a low-carbon grid, solar curtailment is better seen as a problem of insufficient flexibility (via storage or conventional generators), not “too much solar.”

Conventional coal typically can’t ramp up or down quickly...in many cases it takes hours, or sometimes even the better part of a day for older plants. It is the lack of flexibility that leads to curtailment of assets you ideally don’t want to curtail...like renewables. When solar performance peaks at noon, you need other assets to be able to rapidly ramp down to make room. Not incidentally, the new Chinese coal plants being built these days are capable of flexible operations, and older plants are being retrofit to do the same.

Finally, there are no “shortages at night” because of solar only working during the day. System operators plan for the sun not shining...

3) Mischaracterization

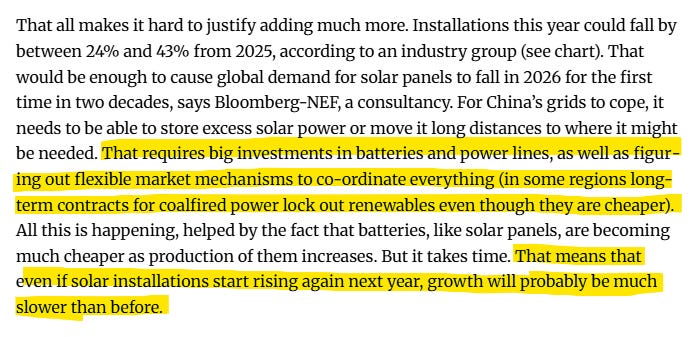

I don’t agree with the characterization that “long-term contracts for coal-fired power lock out renewables even though they are cheaper”. It’s more complex and nuanced than that.

Long-term contracts for anything can lock out anything not contracted. This is less of a question of “coal vs renewables” and more “forward contracting vs real-time markets”.

This is a fundamental friction in power markets. Electricity is contracted ahead of time but dispatched and consumed in real time. You forecast load as best you can when you contract, but when it comes to dispatch, you have to match actual load with actual generation...and forward-contracted generation typically runs first. If total contracted generation exceeds load, then the system must deviate from contracts, typically by allocating curtailment proportionally.

I’d like to see the Chinese power market move away from such high reliance on annual contracting and more use of spot market price signals - and it’s going in that direction. But this can also highlight another problem: renewables often need long-term contracts to get assets financed in the first place and would never want to be reliant on spot market offtake.

Whatever workable balance China ends up with, it’s going to be achieved slowly, via trial and error.

Finally, given the current buildout of storage, UHV, and flexible generation, it’s not clear why solar installs couldn’t re-accelerate in 2027-2028. Renewable consumption quotas are only rising each year, including for data centers, so demand is only going to keep rising too.

4) Misattribution of Intent

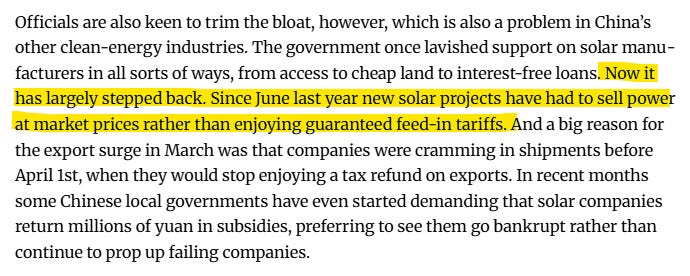

While these details are broadly correct, I wouldn’t frame this as evidence that officials are trying to curb a bloat in solar projects. Renewable subsidies and guarantees have been gradually stripped away over the last decade, well before current market conditions.

The big policy change last year (the infamous Document 136) that shifted projects out of the guaranteed FiT scheme and into CfDs or fully market-based compensation is a continuation of long-running market liberalization trends.

Local officials aren’t anti-solar per se; they just don’t want to see rising curtailment rates (one of their KPIs). They are increasingly incentivized towards approving new projects with clearly identified offtake.

5) Misstatement of Impact

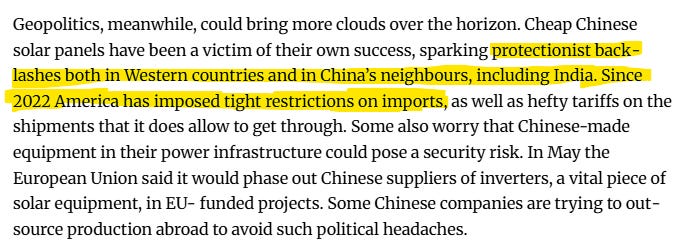

The US hasn’t been a major direct destination of Chinese solar exports since the early 2010s. The major export market has historically been the EU, not the US.

Inverters are not solar panels and the EU remains a big export market for Chinese solar.

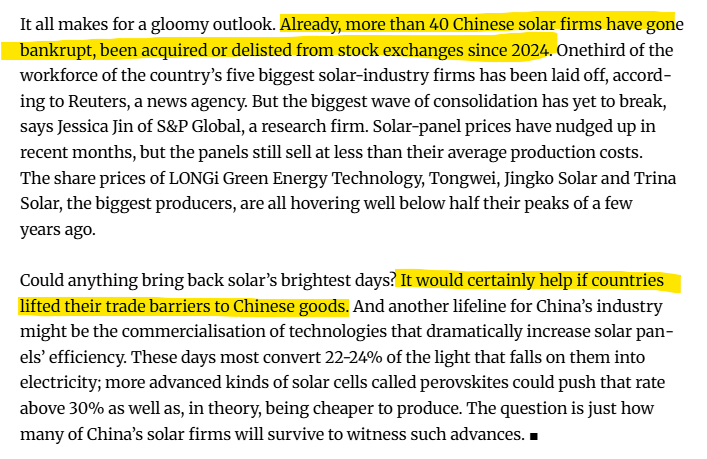

6) Missing the Solution For the Problem

By the logic of this article so far, 40 solar companies going under should be cause for optimism, not a sign of “gloom”. If oversupply is the driving problem, then consolidation of the sector via producer exit is part of the solution, no?

This section also starts to mix up two groups with opposing incentives: Solar panel producers and solar panel buyers (i.e., developers). The former wants higher prices; the latter wants lower prices. Anything that benefits one side on price is going to hurt the other group. These two segments should not be collapsed into the same commentary.

Expanding back into blocked export markets likely doesn’t fix this, even if they were big markets (and considering the successful efforts to cultivate new export markets and triangulate Chinese products via third-country production sites, it’s not even clear how meaningful the blocks have been).

Also, developing export markets are no guarantee of profitability. For solar OEMs, oversupply brings the same vicious price competition in overseas markets. Higher volumes don’t help that much if margins are still extremely thin - and they hurt if margins are negative.

In Closing:

Stepping back, the biggest issue with the piece is that it never really lands on a thesis. It puts together a set of negative data points like falling prices, curtailment, project delays, and pressure on firms, but never explains what ties them together or what it all means.

Most crucially, it never acknowledges that most of these tensions aren’t even particularly weird. They’re the basic mechanics of power markets integrating renewables. Electricity is contracted ahead of time but delivered in real time. Low marginal cost generation smashes prices during peak performance hours. Flexibility always lags capacity. Financing depends on long-term certainty that markets don’t naturally provide. If you don’t know how to anchor the analysis in those facts, I suppose pretty much everything starts to look like chaotic dysfunction.

What’s actually happening is much simpler. China is scaling solar to a level where abundance, not scarcity, becomes an actual binding constraint. The whole sector is getting pulled out of policy protection and into market exposure. Of course that produces friction. It’s supposed to.

You can call it “turmoil” if you want. But this is what it looks like when a sector stops being policy-supported and starts behaving like a real market system.

Thanks for reading.

Just in general, it's best to disregard pretty much anything The Economist has to say about China. They also recently did a botch job on China's auto industry with the brilliant line "...BYD has lost its spark". Hmmm... It's probably a good thing that nobody gets a byline; in the future, they can disavow ever having been involved.

A excellent piece from someone clearly more knowledgeable about the topic than the author of the Economist article.

There seems to be a growing body of such content in major economic and financial publications — cherry-picking data points, or sometimes simply an individual's opinion, to support a negative view of China.

Granted, not everything is working perfectly in the country; yet the economic fundamentals show a system that, on a relative basis, appears to be moving in the right direction compared to the US or EU. What we are witnessing might be called "CDS"; China Derangement Syndrome.